April 2023 Market Update:

A Deep Dive into CNR’s Economic and Investment Outlook

US Economic Momentum Slowing

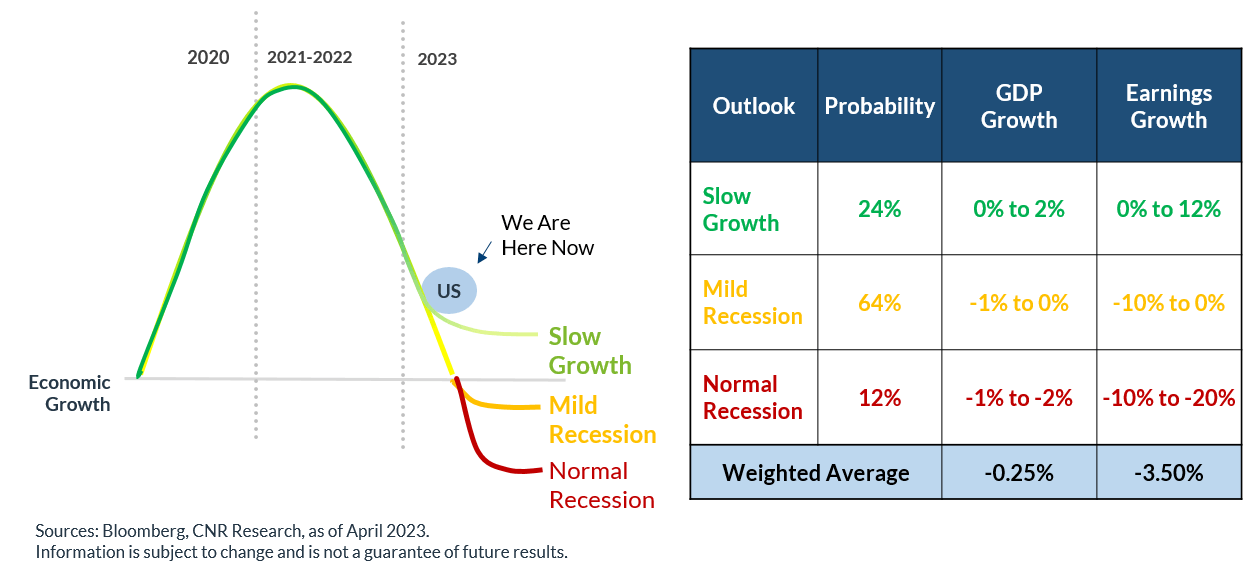

The US is likely to fall into a mild recession during the third or fourth quarter of 2023, according to a market update presented by CNR's leadership team.

The economy is already beginning to slow because of the disappearance of stimulus money from the pandemic and tightening measures implemented by the US Federal Reserve, according to Paul Single, managing director, senior economist and senior portfolio manager at City National Rochdale.

Despite the likelihood of a mild recession, the positive news is there's nothing broken in the US economy. Both household and corporate finances are generally healthy, and there is no indication of a pending deep recession, Single said

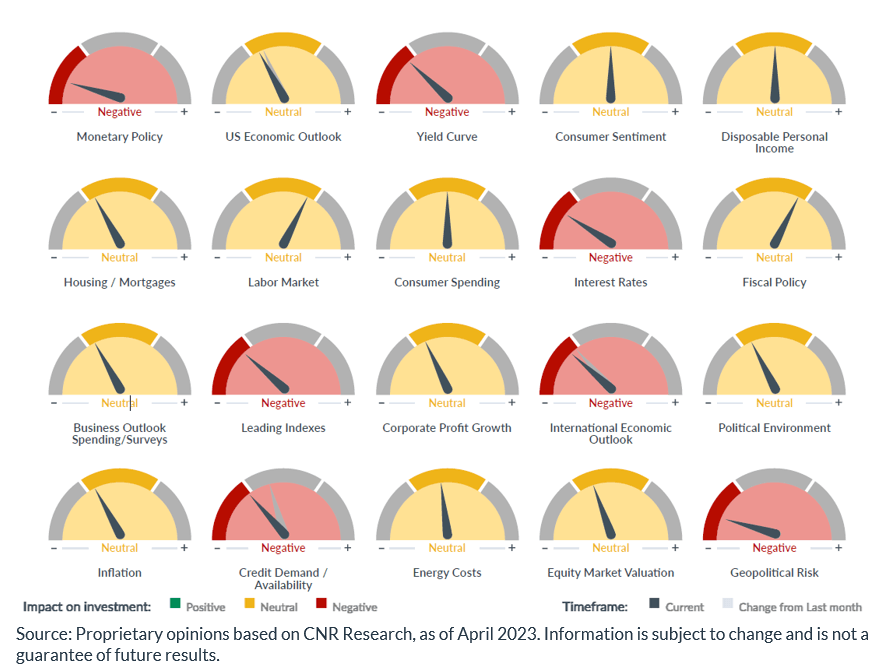

CNR Speedometers®, which are forward-looking indicators for the next six to nine months, are all yellow or red this month. Approximately one-third of the speedometers are negative (red), which signifies the slowdown occurring because of higher inflation, higher interest rates and tightened access to credit.

Recession Risk Continues to Increase

While the probability of a mild recession is far higher than a period of slow growth or a more normal recession, CNR's economists raised the probability of a normal recession up to 12%, compared to our 10% probability in March. Single explained that the risk is slightly higher this month because of the uncertainty around the banking industry and expectations of tighter credit impacting broader economic activity.

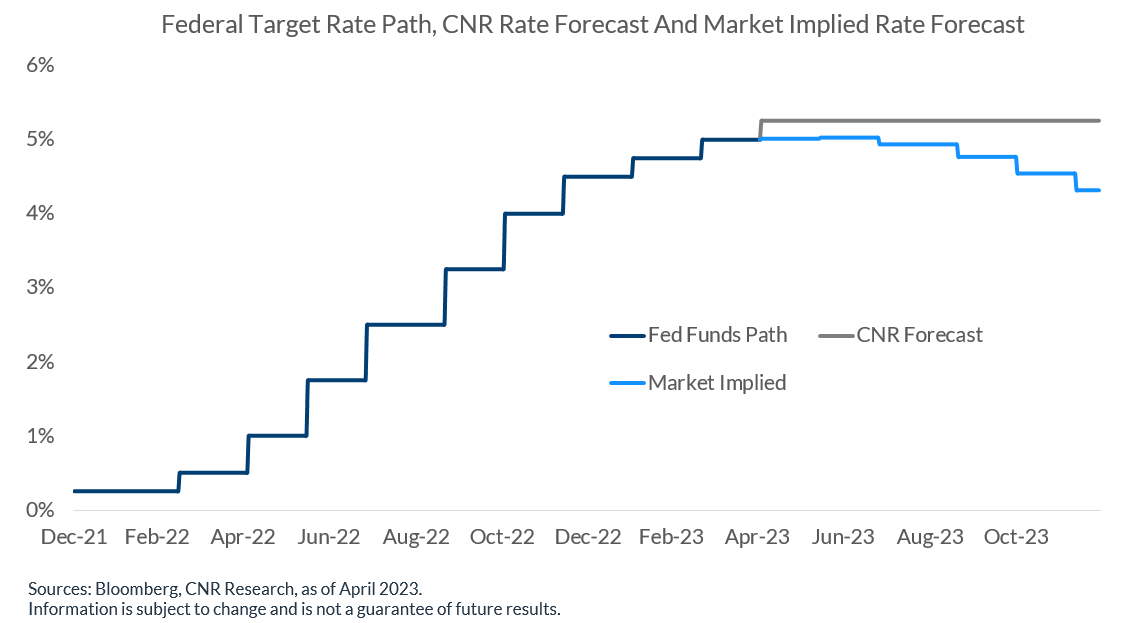

CNR's analysts expect that the Fed rate hikes are approaching an end. However, normalizing monetary policy and eventual easing will take more time and will require inflation to show a more meaningful decline closer to the Fed target rates.

Banking Stresses & the Economy

The biggest impact on the economy from bank stress will come from tightening credit conditions, especially since the US economy significantly relies on credit. Lending standards have already tightened significantly and are expected to tighten further as bank deposits — an important source of funding for banks — continue to decline.

Commercial Real Estate Is a Concern for Banks

Overall, the commercial real estate market is the third largest asset market, with $23.5 trillion in the second quarter of 2022, according to the Federal Reserve. This compares to $53 trillion in residential real estate and $46.5 trillion in equities. Concern about the underlying collateral for commercial real estate loans is higher for smaller regional banks.

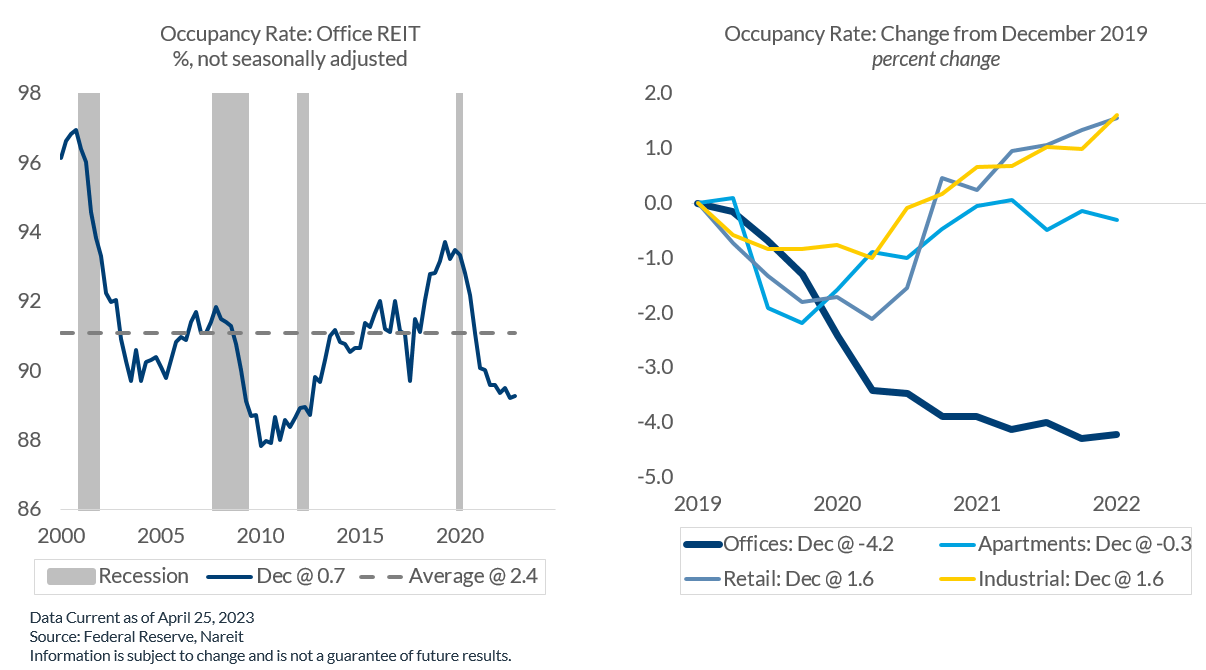

Office real estate is the biggest area of risk for banks, primarily because of the fundamental change in occupancy rates in office spaces since the pandemic drastically accelerated remote work. Office occupancy rates are lower in some locations than others, primarily in California and New York City.

Despite these concerns, CNR doesn't expect the situation with commercial real estate to spark a broader crisis in the banking system.

The Strength of the Dollar

"The dominance of the dollar as the world's global currency has declined since the 1960s, when it accounted for 88.2% of global reserves, versus roughly 60% today", said the Chief Investment Officer for City National Rochdale. However, most of that decline occurred after the introduction of the euro in 1999. Since then, the dollar's status as a global reserve has actually remained remarkably stable, declining only a few percentage points.

Dollar strength moves in mini cycles with ebbs and flows. Recently, its strength has been driven by higher relative interest rates. A modest decline in the strength of the dollar may occur in the next year or two, with greater convergence of interest rates in major economies as the Fed hiking cycle ends.

“After this decade of dollar dominance and dollar strength, we do think that a moderate cyclical decline is likely and is unfolding," he said.

The move to greater dollar diversification is slowly happening, particularly with China, but it will take a long time. For now, the dollar remains dominant and the most viable global reserve currency.

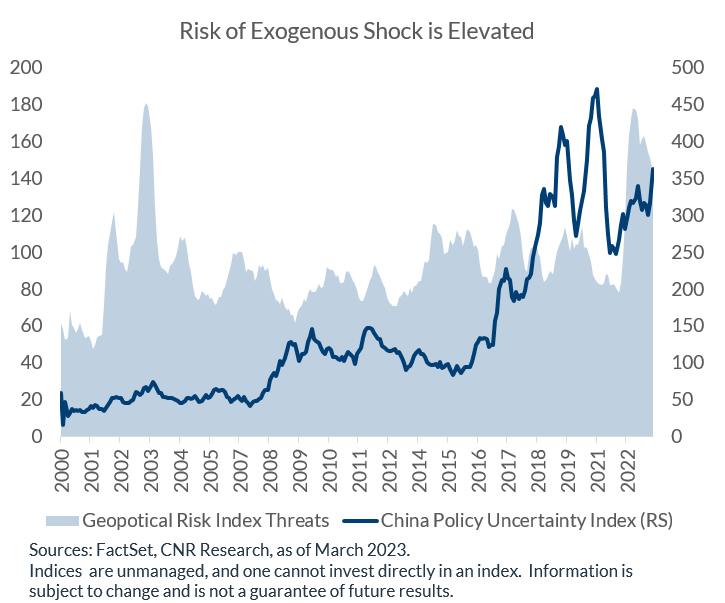

Geopolitical Risks Continue to Impact Markets

Geopolitical risks remain elevated with the potential for another exogenous shock as economic momentum slows.

“We're keeping our eyes wide open because geopolitical uncertainty is high," said the CIO.

CNR remains underweight on China and Europe.

China's reopening is boosting growth, but there are questions about the sustainability of its consumer recovery and other structural challenges.

Europe's economy has performed better than expected, but this is likely a temporary boost due to lower energy prices from a mild winter. Headwinds are still stiff, particularly with inflation and the European Central Bank's lagging policies to address it, especially when compared to the Fed's aggressive actions.

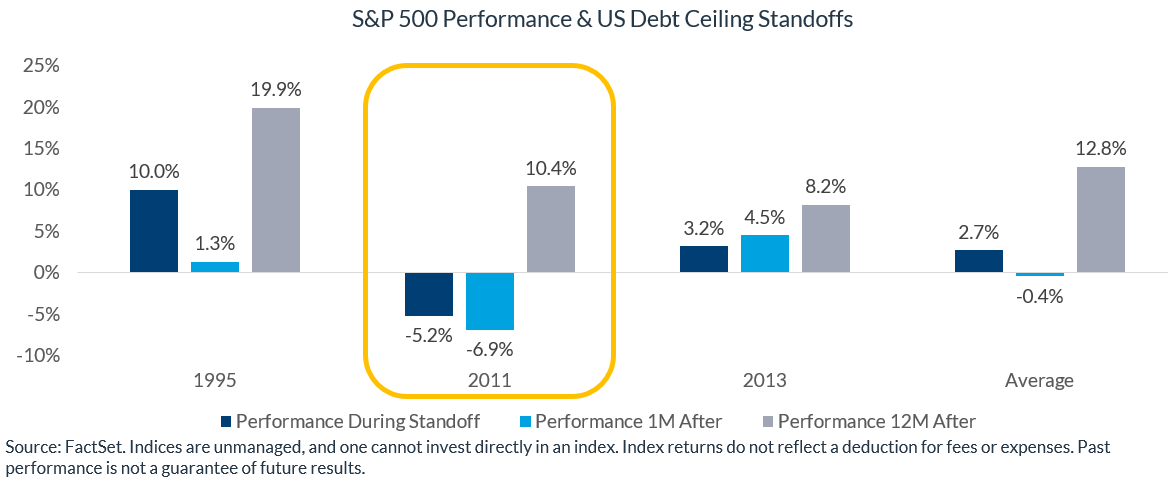

Debt Ceiling Remains a Central Concern

The ongoing debate over the debt ceiling is a concern for CNR, particularly because of the gap between Republicans and Democrats on the issue. Additionally, lower tax receipts in 2023 could accelerate the timeline for when the federal government runs out of cash.

Fitch Ratings, Inc., one of the "Big Three" American credit ratings agencies, has recently threatened to downgrade US debt. While CNR does not believe the US government will default on its debt, the issue could be another source of market volatility in the near term.

Although markets typically do well after debt limit issues, as seen in 2011, there is potential for a significant pullback in stock prices as the deadline to lift the ceiling approaches, especially as a resolution between political parties continues to be elusive.

Other Market Influences to Watch for 2023

CNR's investment team believes that equity valuations continue to be too high and that the markets don't reflect the economic risks ahead. While first quarter earnings have been better than expected so far, this has primarily been due to the bar already having been significantly lowered, he said.

Further downward revisions to earnings expectations could be a catalyst for additional equity declines ahead, he said.

After one of the worst years in history, fixed income markets have rebounded in 2023. CNR remains optimistic about fixed income, particularly because of the yield available across categories to meet different client investment objectives and the diversification benefits that bonds historically provide to portfolios.

Despite the decline in 60/40 portfolio yields in 2022, CNR believes a balanced framework still provides a strong and proven option for investment returns. It's very rare for this type of portfolio to have two consecutive down years, and the investment team remains optimistic for 2023, especially since both stocks and bonds are off to a strong start so far.

However, stocks face a more challenging path forward from here, especially as the economy weakens and potentially enters a mild recession.

While CNR believes that the Fed is coming close to the end of its tightening phase, they continue to believe defensive positioning in investing is the most prudent course given growing recessionary pressures, ongoing geopolitical risks, the debt ceiling standoff and uncertainties around the banking system. The team remains modestly underweight on equities, overweight on fixed income and focused on high quality US stocks and bonds.

Important Information

City National Bank provides investment management services through its wholly owned subsidiary City National Rochdale, LLC, a registered investment advisor. Content from the April 26, 2023 presentation, "Market Update" is reprinted by permission from City National Rochdale.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell, any of the securities mentioned herein.

This document may contain forward-looking statements relating to the objectives, opportunities and future performance of the US and global markets generally. Forward-looking statements may be identified by the use of such words as: “expect,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to, general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. In addition, certain information upon which assumptions have been made has been provided by third-party sources and, although believed to be reliable, the information has not been independently verified and its accuracy or completeness cannot be guaranteed. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of City National Rochdale nor any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

This information is not intended as a recommendation to invest in a particular asset class, strategy or product.

The information presented is for illustrative purposes only and based on various assumptions which may not be realized. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used have been stated or fully considered.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

Concentrating assets in the real estate sector or REITs may disproportionately subject a portfolio to the risks of that industry, including the loss of value because of adverse developments affecting the real estate industry and real property values. Investments in REITs may be subject to increased price volatility and liquidity risk; concentration risk is high.

The yields and market values of municipal securities may be more affected by changes in tax rates and policies than similar income- bearing taxable securities. Certain investors' incomes may be subject to the Federal Alternative Minimum Tax (AMT), and taxable gains are also possible.

Investments in the municipal securities of a particular state or territory may be subject to the risk that changes in the economic conditions of that state or territory will negatively impact performance. These events may include severe financial difficulties and continued budget deficits, economic or political policy changes, tax base erosion, state constitutional limits on tax increases and changes in the credit ratings.

The Standard & Poor’s 500 Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent US equity performance.

The Russell 2000® Index is a market capitalization-weighted index measuring the performance of the small-cap segment of the US equity universe and includes the smallest 2,000 companies in the Russell 3000® Index.

The Dow Jones US Select Dividend Index® measures the performance of the top 100 US stocks by dividend yield.

The MSCI EAFE (Europe, Australasia, Far East) Index is a free float-adjusted market capitalization weighted index that is designed to measure developed equity market results, excluding the US and Canada.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market results in the global emerging markets, consisting of more than 20 emerging market country indexes.

The Bloomberg US Aggregate Bond Index measures the performance of investment grade, US dollar-denominated, fixed-rate taxable bonds.

Bloomberg US Investment Grade Corporate Bond Index. The Bloomberg US Investment Grade Corporate Bond Index measures the performance of investment grade, corporate, fixed-rate bonds with maturities of one year or more.

The Bloomberg US Corporate High Yield Index measures the performance of non-investment grade, US dollar- denominated, fixed-rate, taxable corporate bonds.

The Bloomberg US Municipal Bond Index measures the performance of investment grade, US dollar-denominated, long- term tax-exempt bonds.

The Bloomberg Municipal High Yield Bond Index measures the performance of non-investment grade, US dollar-denominated, and non-rated, tax-exempt bonds.

CNR is free from any political affiliation and does not support any political party or group over another.

Non-Deposit Investment Products: • Are Not FDIC Insured • Are Not Bank Guaranteed • May Lose Value