Economic Perspectives: Mid Year Review

Markets have had every reason to wobble over the past month, yet they’ve remained remarkably resilient. Tensions between Israel and Iran flared again in June, with military escalations drawing global concern, but the market did not crack. Volatility has eased and equity markets remain a steady testament to just how well the current economic environment is absorbing external shocks.

On the domestic front, Washington has inched closer to a significant fiscal milestone. The Senate has passed the budget reconciliation bill, which includes modifications to the SALT cap, renewable energy tax credits, Medicaid provisions, and regulatory rollbacks. It also makes the tax cuts from the Tax and Jobs Act of 2017 permanent.

With the framework in place, the implications for taxes, spending and ultimately the broader economy will be felt in the second half of this year. Against this backdrop of geopolitical stress and legislative activity, markets have stayed surprisingly steady.

It’s a reminder that while headlines capture attention, the underlying fundamentals still matter, and for now, they continue to show stability.

So this month, the committee left its speedometer dial settings unchanged. While we’ve seen some new developments on tariffs, inflation and regulation, many of the impacts are still playing out. Rather than make changes prematurely, we’ve opted to wait for more definitive data before adjusting position.

Despite no changes, we did focus on four key areas this month: geopolitical risk, equity market valuation, the energy risk premium and fiscal policy.

■ Previous Month ■ Current Month

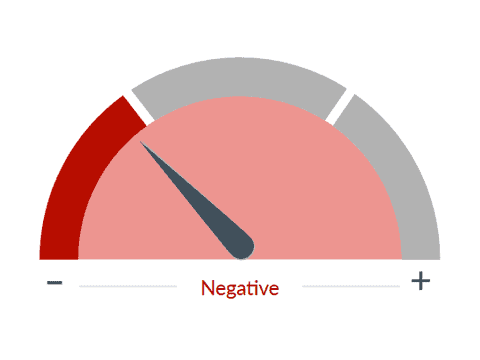

Geopolitical Risk

What we see

Geopolitical risk examines how geography and economics influence politics and international relations. Geopolitical risk includes the risk associated with international policy, trade, and global financial market stability, as well as wars, terrorist acts, tensions between states, and other events that can impact the normal and peaceful course of international relations.

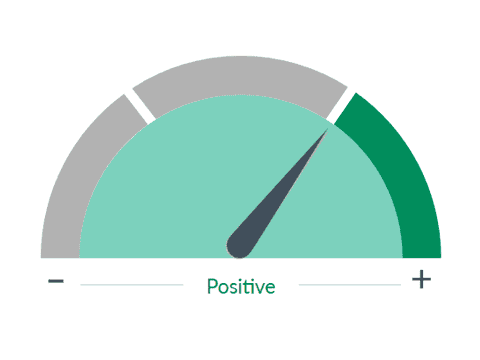

Dial 1: Geopolitical Risk, 1:47— First, geopolitical tensions do remain elevated, but they are lower than the peaks we saw just a few weeks ago. The market response to the Israel–Iran conflict has been orderly and measures of volatility have declined. However, there’s still an elevated probability of surprise, particularly with the U.S. election cycle heating up. The Trump administration’s approach reintroduces a higher degree of geopolitical unpredictability.

Trump’s willingness to act decisively and at times abruptly raises the tail risk of sudden events with market implications. And that uncertainty is part of our thinking and keeping the geopolitical dial unchanged for now, despite some easing of tension.

■ Previous Month ■ Current Month

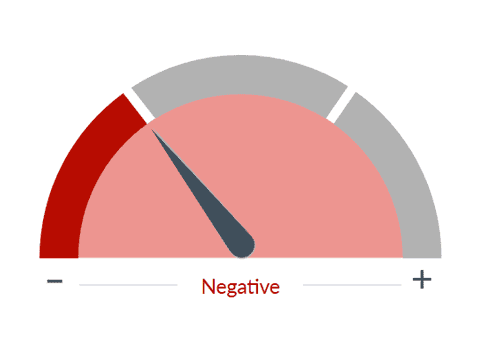

Equity Market Valuation

What we see

Questions of value are always subjective and relative. We believe that equity market valuation should be measured against both the value of stocks at their historical levels and the other investment options available. A stock is worth its future earnings, but that involves a degree of uncertainty, which affects its price depending on the degree. In addition, investors have many other asset classes to choose from, including corporate bonds, Treasury bonds, alternative investments, and the like. We look at all of these factors before we determine what we believe to be a fair equity market valuation.

Dial 2: Equity Market Valuation, 2:25— Second, equity valuations remain elevated. The overall market is still expensive by historical standings. During our recent investment committee meeting, we noted that U.S. equity valuation is well above fair value. That keeps this dialing red. When we look at corporate earnings outlooks, they have come down modestly even as market optimism has held firm. We continue to believe valuations are high historically, but if inflation remains tame and policy clarity improves, there could be some runway for the market to continue rising.

■ Previous Month ■ Current Month

Energy Costs

What we see

Significant changes in energy/oil prices can have important but differing impacts on the overall economy. Higher energy prices act as a tax on consumers and businesses, absorbing money that would normally be used to buy other goods. However, they can also boost production and investment in the mining and energy sectors of the economy. Lower energy prices can increase consumer spending and lower manufacturing costs.

Dial 3: Energy Costs, 2:55— Third, energy markets quickly priced in the geopolitical risk premium following the news of the attacks on Iran.

Disruptions to oil infrastructure and shipments do impact prices. However, the market reaction to recent geopolitical escalation is in line with historical reactions.

This suggests that the impact on oil prices and the markets more broadly will continue to dissipate.

That being said, oil prices are higher than they were before the event occurred, but they have dropped significantly from their peaks.

We’ve also seen an uptick in capital spending among energy companies, especially those supporting the AI-driven data center build-out. But the sector remains sensitive to further geopolitical developments. So this is a fluid situation and the energy dial reflects that.

■ Previous Month ■ Current Month

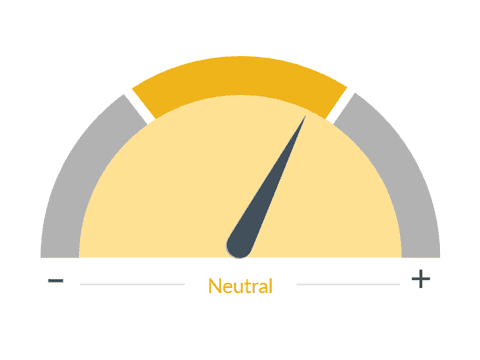

Fiscal Policy

What we see

Changes in tax rates, regulation, and government spending affect the decision-making process of consumers and businesses. By changing tax laws, the government can effectively modify the amount of disposable income available to taxpayers or raise the costs for businesses. However, this process takes time, as the money needs to wind its way through the economy, creating a significant lag between the implementation of fiscal policy and its effect on the economy.

Dial 4: Fiscal Policy, 3:37— Fourth, the fiscal outlook has entered a more active phase. The passage of the budget reconciliation bill marks a shift, one from stalled rhetoric to tangible legislation.

The bill includes changes that could spur capital investment and provide targeted support to consumers. In parallel, we’re watching the July 9 tariff extension deadline. Tariff negotiations remain in flux, taking longer than initially expected. While agreements have been reached with China, the U.K. and Vietnam, many countries do not yet have a trade deal in place as the deadline approaches.

Companies are adjusting their supply chains and pricing strategies, but the full inflationary and economic impact won’t be clear until these policies settle. Until we get that clarity, we’re holding this dial steady as well.

So where does this leave us as we enter the second half of 2025? For starters, the market has shown surprising composure amid high levels of non-market stress. That resilience is encouraging, but we remain alert to shifting risks. The next few months will be critical for determining the impact of tariffs on inflation and we think the areas to watch remain oil prices, long-term interest rates and the U.S. dollar’s reaction to policy. A reacceleration in inflation could keep the Fed on the sidelines, putting pressure on the market, but we still see one to two cuts. We also expect to continue to see structural pressure on long-term rates and that’s driven by deficits and inflation expectations.

That could reshape risk premiums across asset classes, although we view rates above 4.5% as a low probability at the time of filming. So the bottom line is while the foundation remains stable, the second half of this year will undergo major shifts impacting inflation, fiscal execution, Federal Reserve activity and global risks. We continue to believe this is a time for selectivity, diversification and active risk management.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

CNR Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect City National Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

City National Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and City National Rochdale are subsidiaries of Royal Bank of Canada.

©2025 City National Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE