Tracking 2025 Tax Legislation

One Big Beautiful Bill Act

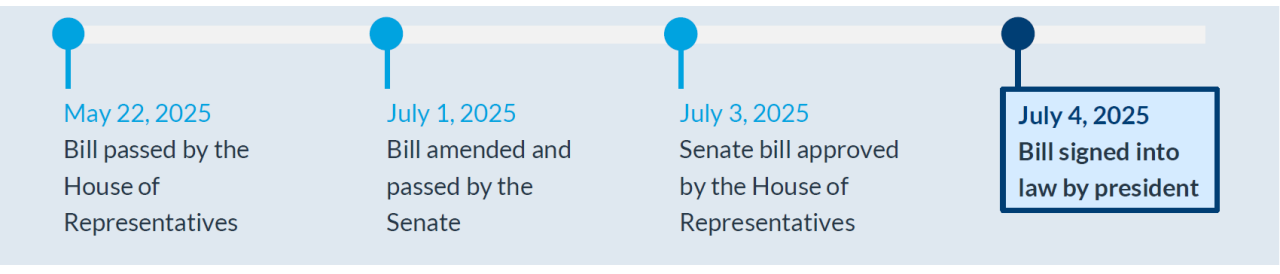

On July 4, 2025, President Trump signed into law the One Big Beautiful Bill Act (OBBB). The OBBB significantly modifies much of the tax code, addressing many of the expiring tax provisions from the 2017 Tax Cuts and Jobs Act (TCJA), and includes additional changes to the tax code impacting individuals, estates, trusts and businesses. Most provisions will go into effect between January 1, 2025, and January 1, 2026.

BUDGET RECONCILIATION

Like the TCJA, the OBBB was passed via budget reconciliation, a process that allows certain budget-related bills to pass through Congress via simple majority and requires the bill to not increase the federal deficit beyond a certain timeframe. While some of the OBBB provisions are permanent changes to tax law, others are scheduled to expire (sunset) at some point in the future.

OBBB LEGISLATIVE TIMELINE

SUMMARY OF KEY PROVISIONS AFFECTING INDIVIDUALS, ESTATES AND BUSINESS OWNERS

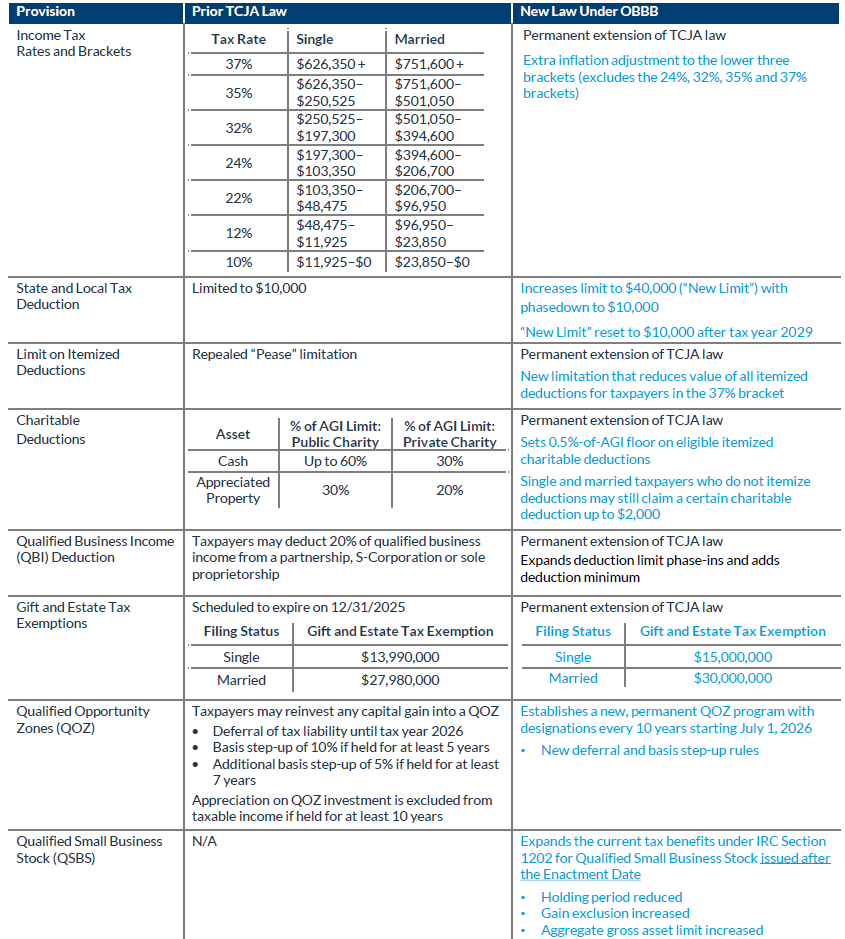

- Permanently extends TCJA individual income tax rates and brackets (certain exceptions for the 24% to 37% brackets)

- Temporarily increases limit for state and local tax (SALT) deduction, subject to phasedown based on modified adjusted gross income (MAGI)

- Introduces permanent percentage reduction of itemized deductions for taxpayers in the 37% bracket

- Permanently extends the maximum 60% of AGI limitation for charitable contributions to public charities (plus other changes and limitations for charitable deductions)

- Permanently extends the TCJA qualified business income deduction

- Permanently increases the estate, gift and generation-skipping transfer (GST) exemptions

- Renews and modifies qualified opportunity zone (QOZ) program

- Expands the qualified small business stock (QSBS) tax provisions under IRC Section 1202

COMPARISON OF KEY PROVISIONS

Prior Law Under the Tax Cuts and Jobs Act (TCJA) vs. Current Law Under the One Big Beautiful Bill Act (OBBB)

Blue text denotes changes made to prior law by the OBBB

ONE BIG BEAUTIFUL BILL ACT

INDIVIDUAL TAX PROVISIONS (as of July 4, 2025)

Permanent Extensions: The following provisions of TCJA are made permanent by the OBBB and include some additional changes to prior TCJA law.

INDIVIDUAL TAX PROVISIONS (as of July 4, 2025)

Permanent Extensions (continued): The following provisions of TCJA are made permanent by the OBBB and include some additional changes to prior TCJA law.

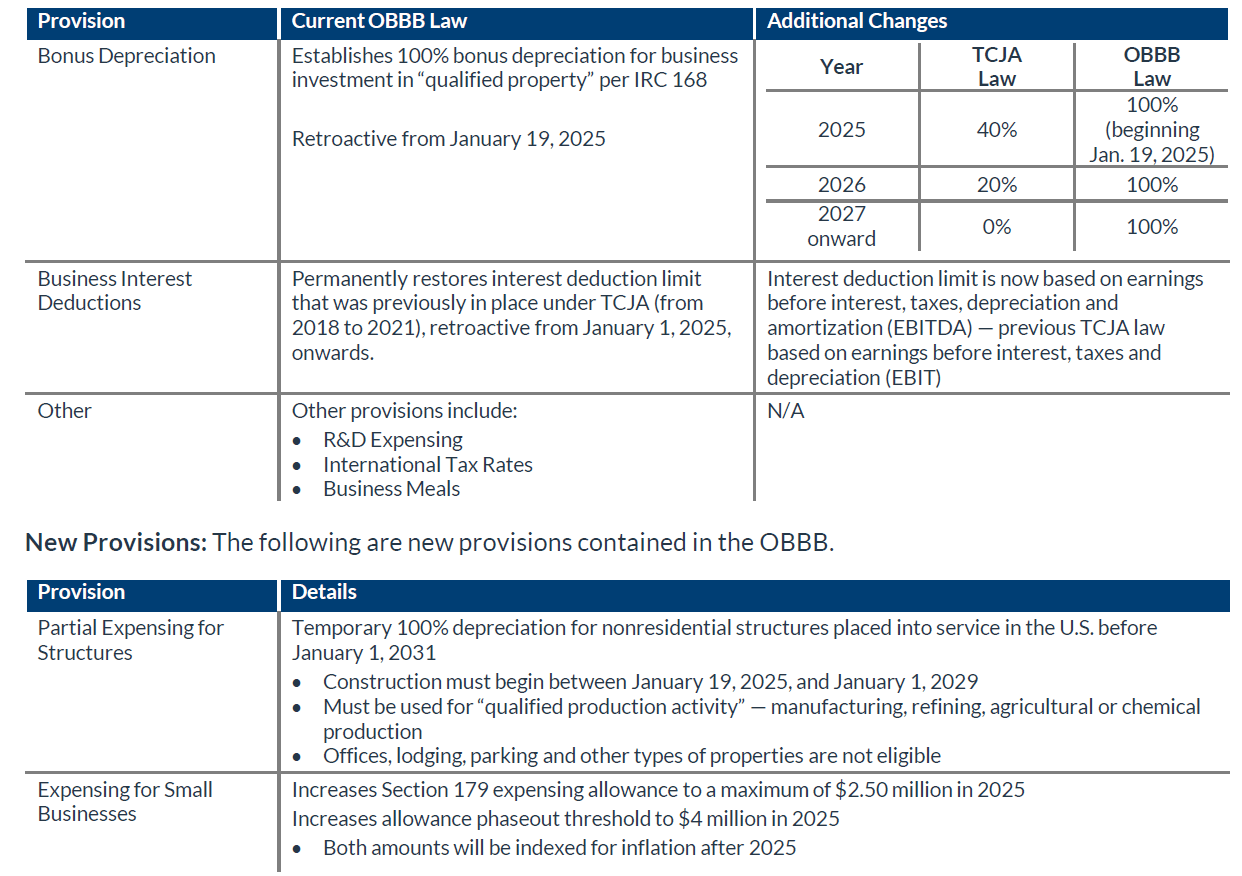

BUSINESS TAX PROVISIONS (as of July 4, 2025)

Permanent Extensions: The following provisions of TCJA are made permanent by the OBBB and include some additional changes to prior TCJA law.

OTHER NOTABLE PROVISIONS

The OBBB contains additional provisions not noted above. Some of these provisions are:

- Information reporting

- Additional tax cuts

- Low-income housing tax credit

- Clean fuel production

- Modification of various international tax provisions

- Changes to tax rules for foundations, colleges, universities and other tax-exempt organizations

- Changes to clean energy tax provisions

- Net operating losses for pass-throughs

- Employee retention tax credit

HOW DOES NEW TAX LEGISLATION AFFECT YOU?

The OBBB contains sweeping changes to tax law that may affect individuals, estates and businesses. Taxpayers should work with their financial, tax and legal advisors to understand how the OBBB may affect their tax profile and overall financial and estate plan.

RBC Rochdale’s Private Wealth Solutions team specializes in educating and assisting clients with analyzing and making important financial decisions with the Comprehensive Wealth Assessment. RBC Rochdale’s Comprehensive Wealth Assessment is a complimentary, holistic service that focuses on identifying gaps and solutions and empowers clients to make informed decisions. We pair sophisticated financial tools and modeling techniques with a personal approach to illustrate for you the financial benefits advance planning can help deliver.

To learn more, contact your Financial Advisor. You can also visit us at www.cnr.com, or email us at citynationalrochdale@cnr.com.

Check out our previous 2 pieces on this legislation below:

1 “Qualified tips” is defined as “cash tips received by an individual in an occupation which customarily and regularly received tips on or before December 31, 2024”

2 “Qualified overtime compensation” is defined as “compensation paid to an individual in excess of the regular rate”

3 “Qualified passenger vehicle loan interest” is applicable for any vehicle (1) which is manufactured primarily for use on public streets, roads and highways; (2) which has at least two wheels; (3) which is a car, minivan, van, sport utility vehicle, pickup truck or motorcycle; (4) which is treated as a motor vehicle for purposes of Title II of the Clean Air Act; and (5) which has a gross vehicle weight rating of less than 14,000 pounds

Important Information

This document is for general information and education only. It is not meant to provide specific tax guidance. The information in this document was compiled by the staff of RBC Rochdale, LLC (RBC Rochdale) from data and sources believed to be reliable, but RBC Rochdale makes no representation as to the accuracy or completeness of the information. The opinions expressed, together with any estimates or projections given, constitute the judgment of the author as of the date of the presentation. RBC Rochdale has no obligation to update, modify, or amend this document or otherwise notify you in the event any information stated, opinion expressed, matter discussed, estimate, or projection changes or is determined to be inaccurate.

RBC Rochdale, as a matter of policy, do not give tax, accounting, regulatory, or legal advice. Rules in the areas of law, tax, and accounting are subject to change and open to varying interpretations. Any strategies discussed in this document were not intended to be used, and cannot be used for the purpose of avoiding any tax penalties that may be imposed. You should consult with your other advisors on the tax, accounting and legal implications of actions you may take based on any strategies or information presented taking into account your own particular circumstances.

This presentation (or any portion thereof) may not be reproduced, distributed, or further published by any person without the written consent of RBC Rochdale.

RBC Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

© 2026 RBC Rochdale. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS: • ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE