2025 Mid-Year Outlook Webinar

A Deep Dive into CNR’s Economic and Investment Outlook

June 26, 2025

June 26, 2025

2025 June Mid-Year Outlook Webinar Summary

Below is a summary, focusing on key insights from the June 26, 2025 Market Update webinar on the economy, financial markets and portfolio implications.

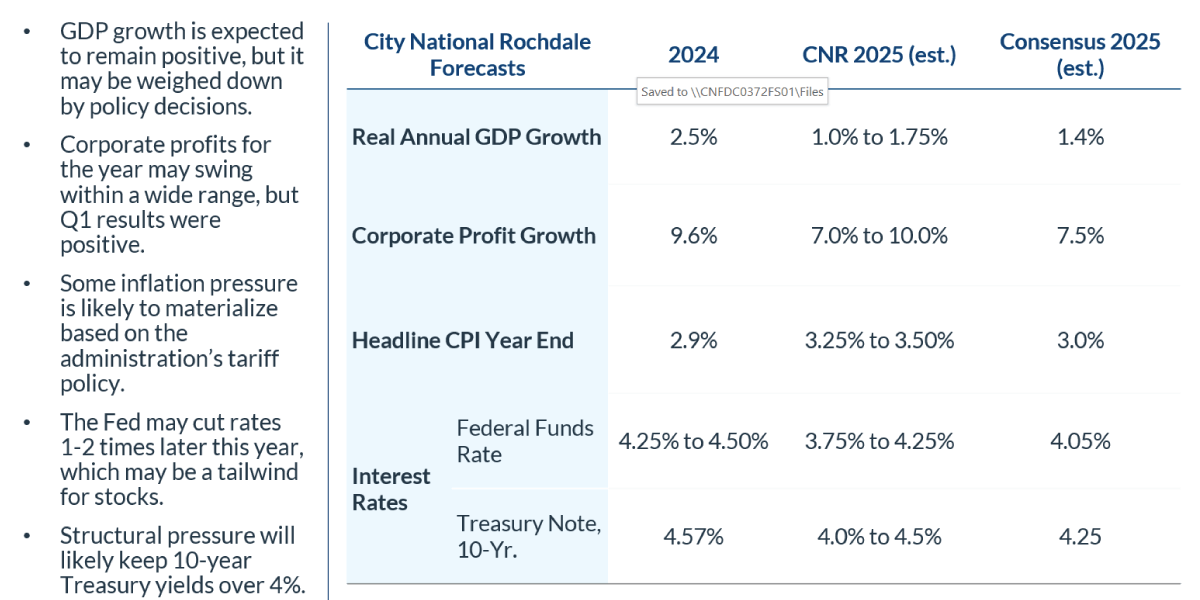

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period.

e: estimate.

The consumer price index (CPI) measures the monthly change in prices paid by U.S. consumers.

Sources: Bloomberg, FactSet, proprietary opinions based on CNR Research, as of June 2025. Information is subject to change and is not a guarantee of future results.

Economic Landscape: Growth, Inflation & the Fed

Slowing Global and U.S. Growth

Inflation Remains Sticky

Federal Reserve Policy

Financial Markets: Cross-Asset Themes

Equities

Fixed Income

Credit & Spreads

Commodities

Portfolio Implications: Strategy & Positioning

Equities

Fixed Income

Credit & Alternatives

Risk Outlook & Scenarios

Persistent Inflation

Growth Shock (Hard or Soft Landing)

Concluding Themes

Summary

This juncture offers a strategic sweet spot: yields have repriced upward, but earnings drivers remain intact. The key is high-conviction, quality-oriented positioning, with liquidity and tactical hedges, against a backdrop of macro complexity. Scenario planning and client education around inflation uncertainty, Fed transition and policy as pivot remain mission-critical.

Review Your Portfolio with Your Financial Advisor Today

City National Rochdale encourages you to review your investment portfolio with your advisor. Contact our financial professionals today to get help with your wealth planning needs.

Definitions

Gross Domestic Product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR), which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice, or a recommendation for any security. It is derived from proprietary and non-proprietary sources that have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy or reliability.

Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and management’s view as of the time of these statements. Accordingly, such statements are inherently speculative, as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification may not protect against market risk or loss. Past performance is no guarantee of future performance.

There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager, or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

There are inherent risks with fixed income investing. These risks may include interest rate, call, credit, market, inflation, government policy, liquidity, or junk bond. When interest rates rise, bond prices fall. This risk is heightened with investments in longer duration fixed-income securities and during periods when prevailing interest rates are low or negative.

Credit risk is the risk that one or more fixed income securities in portfolio will decline in price or fail to pay interest or principal when due because the issuer of the security experiences a decline in its financial status. Credit risk is increased when a portfolio security is downgraded or the perceived creditworthiness of the issuer deteriorates.

Alternative investments are speculative, entail substantial risks, offer limited or no liquidity and are not suitable for all investors. These investments have limited transparency to the funds’ investments and may involve leverage which magnifies both losses and gains, including the risk of loss of the entire investment. Alternative investments have varying, and potentially lengthy lockup provisions.

Indices are unmanaged, and one cannot invest directly in an index. Index returns do not reflect a deduction for fees or expenses.

CNR is free from any political affiliation and does not support any political party or group over another.

© 2025 City National Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS: • ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE