-

Economic Perspectives

Leading Economic Indicators

August 2025

- Filename

- Economic Perspectives AUGUST 2025.pdf

- Format

- application/pdf

TRANSCRIPT

The economy is at a crucial stage. The inflation rate remains above the target level of 2% and tariffs are apt to keep upward pressure on prices. At the same time, the labor market is strong, but demand for new workers is waning. This is forcing the Fed to make some tough choices. Do they keep interest rates on the high side, restricting economic growth in hopes of bringing down inflation to the target? Or do they cut interest rates in an attempt to stimulate demand for workers?

The answer resides in the direction of the economy. Historically, one economic indicator that many have looked at for determining shifts in the direction of the economy is the Leading Economic Indicators Index. This index, as the name suggests, is used by policymakers, businesses and investors to get an understanding of how the economy is progressing through the business cycle. It’s designed to signal peaks and troughs in the business cycle.

The index is published monthly by the Conference Board, which is a nonprofit independent research group. It’s a composite index composed of 10 independent economic indicators. They’ve been carefully selected based on their ability to provide early signals to changes in economic trends.

Leading Economic Indicator Index

index value, % change, seasonally adjusted

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

Chart 1, 1:36– For some background perspective, this chart shows the value of the Leading Economic Index since 1960, with the gray columns representing recessions. The green arrows show the upward trajectory of the index during expansionary times. The index tends to peak about one year ahead of a recession. The red arrows show the reversal in the upward trend, which coincides with the recessionary periods. But in more recent times, for the past three years, the index has been on a downward trajectory. What gives?

Leading Economic Indicators Index

index value, seasonally adjusted

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

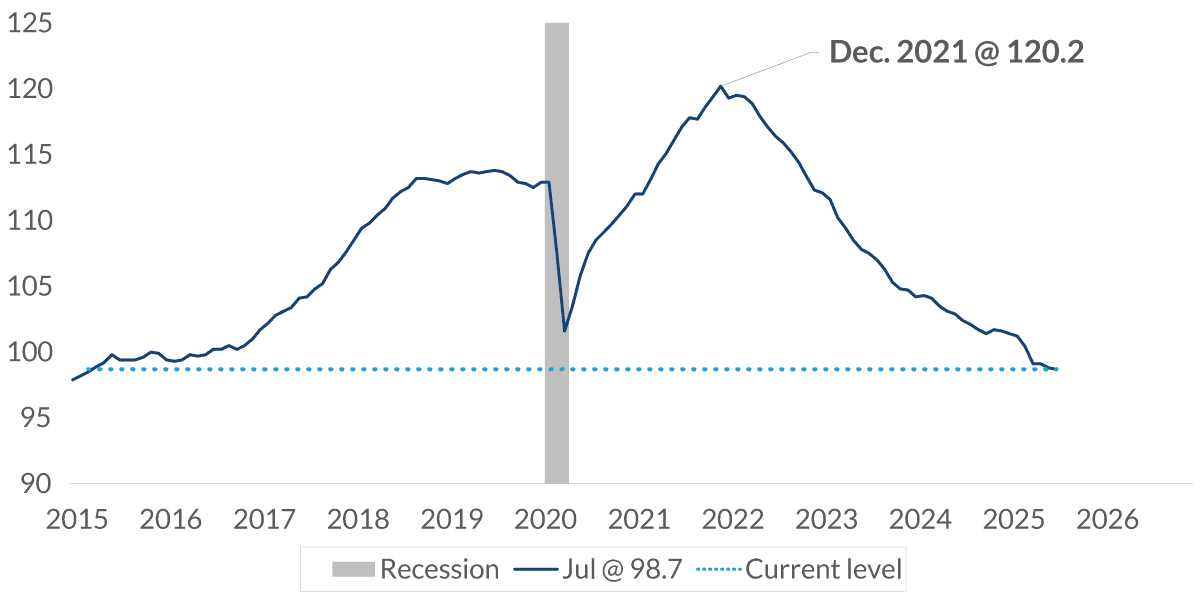

Chart 2, 2:07– This is a more contemporary view of the same index. Here, you can see that the index, at 98.7, is lower than it was during the pandemic and it’s at a level not seen in 10 years.

Leading Economic Indicators Index: Monthly Change

% change, seasonally adjusted

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

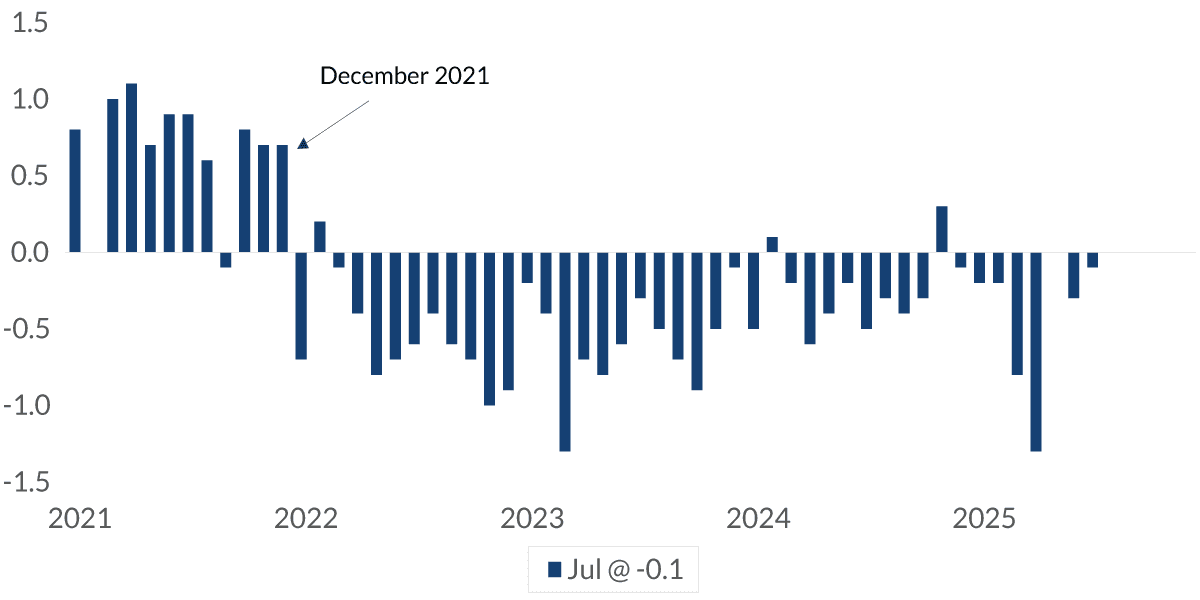

Chart 3, 2:19– This chart offers another perspective by showing the monthly change of the index. Since hitting a peak three and a half years ago, the monthly change has increased just three times. This is, of course, counter to how the economy has performed during the same period of time. Since that peak in December 2021, quarterly GDP has averaged a strong 2.2%. Payroll growth has averaged 227,000 per month for a total of 9.5 million more workers. So what gives? Well, looking at the 10 individual components does provide some insight.

Leading Economic Indicators

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

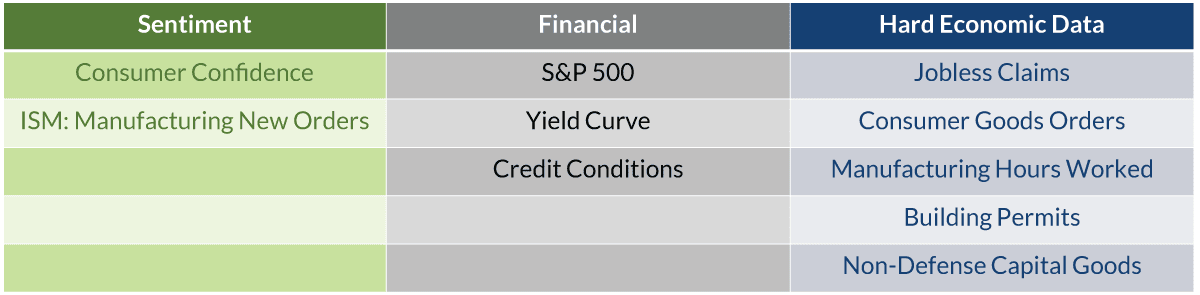

Chart 4, 2:58– Here are the 10 indicators, which we’ve put into three categories. For sentiment in green, we have consumer confidence and the ISM orders for manufactured products. In gray are financial assets: the S&P 500, the slope of the yield curve and credit conditions. And then finally, in blue, hard economic data: initial claims for unemployment insurance, orders for consumer goods, the number of hours worked by manufacturing workers, building permits for homes, and orders for capital goods, excluding defense and aircraft. All 10 of these measures provide a very broad view of the economy.

LEI: Contribution to Performance

%, seasonally adjusted, as of July 2025

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

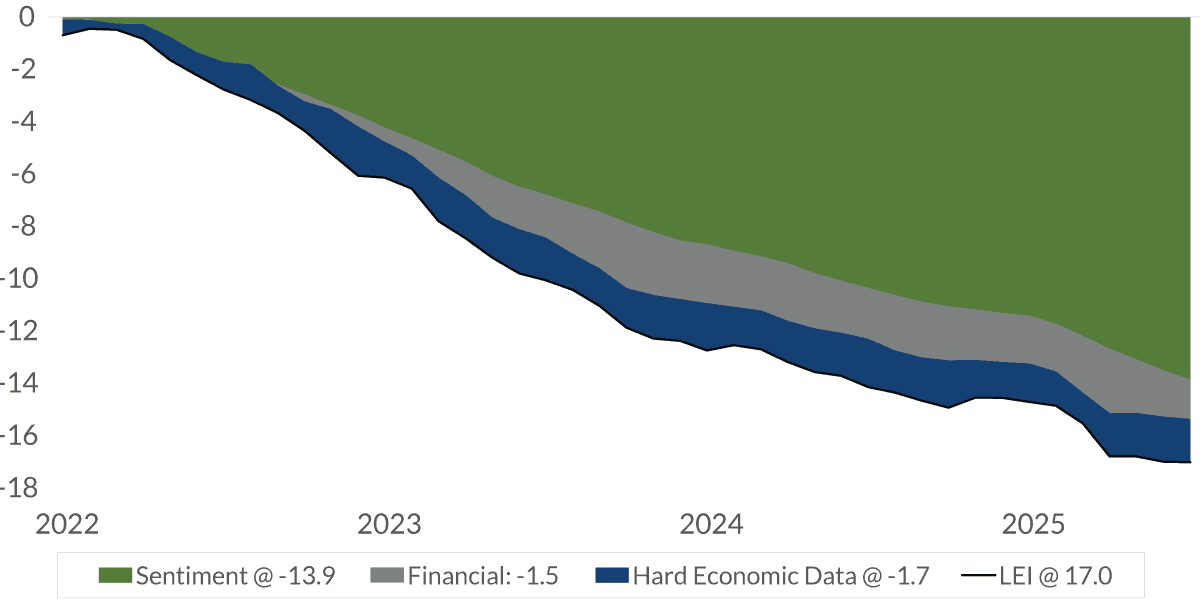

Chart 5, 3:38– This chart shows the aggregate performance of the LEI since 2022. Right after peaking for the month before, the two indicators of sentiment in green accounted for 80% of the decline. Those components have performed poorly post-pandemic and they have a very large weighting in the index.

Leading Economic Indicators Index

contribution to change since start of expansion

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

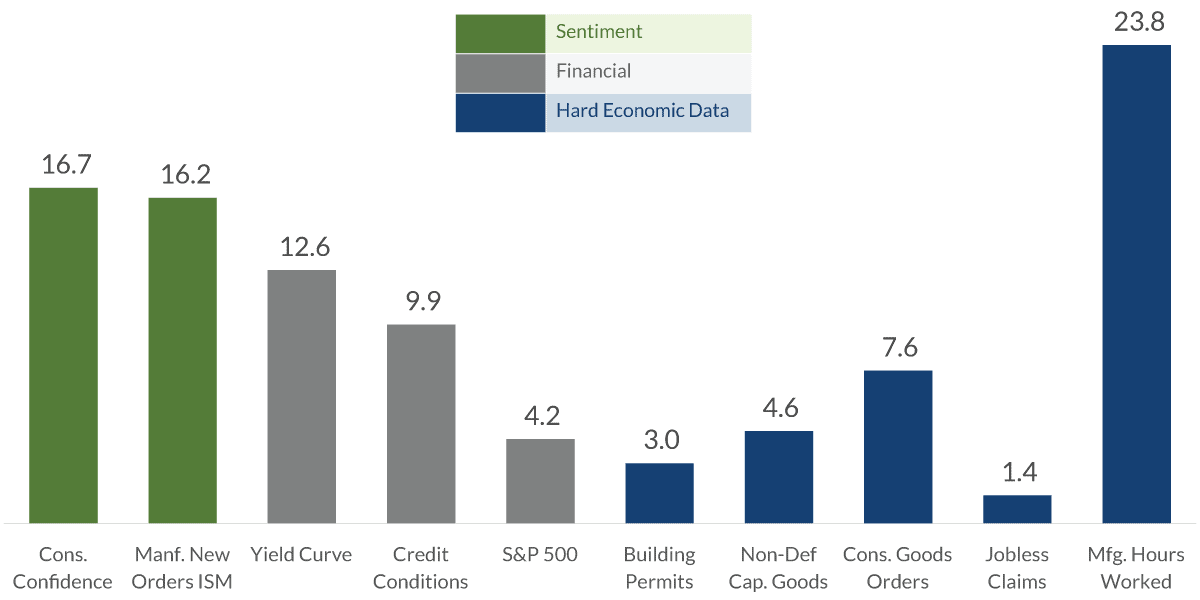

Chart 6, 4:00– This chart shows the weightings of each one of the 10 components. Each component is assigned a weight based on its significance in predicting economic trends. Two sentiment indexes in green account for about one-third of the entire index.

Leading Economic Indicators Index

contribution to change since January 2022

Data current as of August 21, 2025

Source: The Conference Board

Information is subject to change and is not a guarantee of future results.

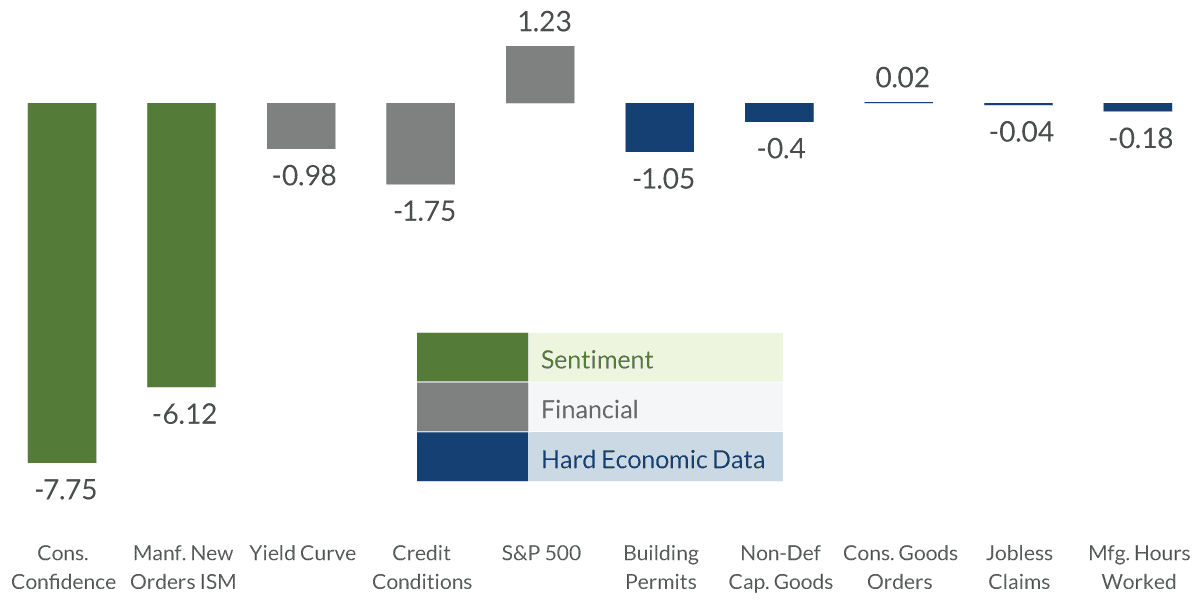

Chart 7, 4:16– This chart shows how each of the 10 components has contributed to the total performance. It is just a simple formula: the performance of each indicator multiplied by its weighting. As we saw earlier, sentiment components have caused the biggest drag. These two sentiment components are considered soft data, which is less reliable than hard data, as consumers and businesses can say one thing and do another.

So why has the Leading Economic Indicators Index been so unreliable of late? Well, first off, forecasting economic trends is challenging. It’s based on assumptions that may or may not always hold true. Also, one thing the LEI does not capture is the influence of external factors, such as geopolitical events, natural disasters, or policy changes, which can all have a significant impact on the economy.

This may be one of the reasons it has not been a reliable indicator of late. Fiscal policy from the federal government has been running massive deficits in the past few years, adding stimulus that is much greater than the economy is accustomed to, especially during periods of peace or economic strength.

Another factor is the public’s attitude since the pandemic. Confidence levels have been very low. This, of course, has been a perplexing trend, considering how strongly the economy has performed since the pandemic, a very low unemployment rate, strong spending, and a booming stock market. It may be attributed to the high levels of inflation from a few years ago. Americans hate inflation, even if they have the money to pay for the higher prices. Now, the public is growing more stressed about the cost of tariffs and other economic policies.

Another reason is the ISM Manufacturing Index, which gives us a good feel of what’s going on in the manufacturing sector. It’s been on a downward trend since peaking in 2020. This is not surprising, since the manufacturing sector has been in a contraction phase as consumers have increased their spending on services rather than goods. Now, LEI can send false signals. It has done so in the past. These false signals were overwhelmingly concentrated on just a handful of components, as is the case right now.

Clearly, the economy has lost momentum this year. That’s seen in reduced business investment and spending by consumers. But much of that is due to economic uncertainty of the public as the administration deals with tariff issues. Despite the recession risk implied in the LEI report — again, driven by just two of the 10 indicators — we at City National Rochdale do not see a recession risk in the near term.

The underlying strength of the economy, as indicated by the low unemployment rate and healthy balance sheets of both households and corporations, will keep economic growth on a positive trajectory, albeit at a less steep pace than what we’ve seen in the past few years.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and management's view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based-on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investment strategies have the potential for profit or loss; changes in investment strategies, contributions or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio.

© 2025 City National Bank. All rights reserved.