Economic Perspectives: Domestic Manufacturing: Making a Comeback?

The key takeaway is: Our confidence in a soft landing for the U.S. economy continues to increase. We have a number of positive shifts to our Speedometers® — we now have seven green, eleven yellow and only two red dials.

■ Previous Month ■ Current Month

US Economic Outlook

What we see

Timely economic forecasting is very difficult to do but extremely important, especially as the significance of economic information to financial markets continues to rise.

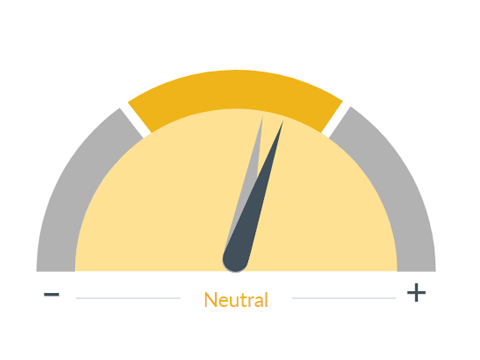

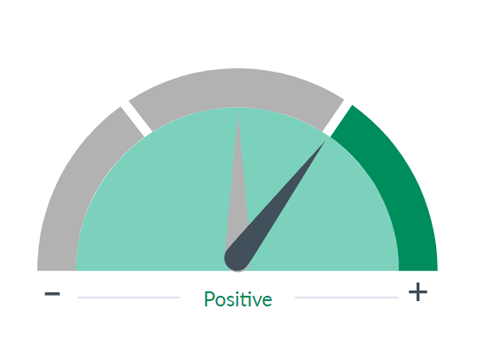

Dial 1: US Economic Outlook 0:29— The U.S. Economic dial moves to the right to reflect lowering our estimated risk of a mild recession to 30% and an increase in our GDP [gross domestic product] forecast to a range, right now, of 1.5%-2.25%. While economic readings in January did show signs of a slowing from the strength in the fourth quarter, most likely due to weather influences and seasonal impacts, the consumer clearly remains resilient.

We’re also seeing positive signals from the manufacturing surveys, combined with the prospects of real consumption tracking to around 2.5% in the first quarter, indicating to us that the U.S. economy is on solid footing.

■ Previous Month ■ Current Month

Leading Indexes

What we see

We look at a number of indices that have a strong track record in anticipating turns in business cycles. These include measures of production, employment, income, and sales, which have a strong correlation to subsequent economic activity.

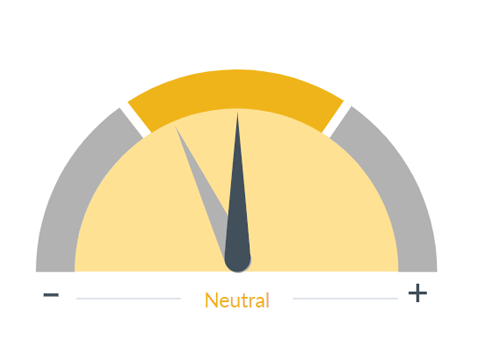

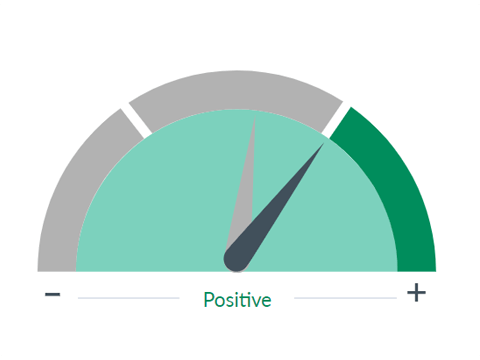

Dial 2: Leading Indexes 1:12— The Leading Economic Indicator Index has also shifted positively to the right. The Conference Board’s Leading Economic Index (LEI) turned positive in February for the first time since December 2021. Encouragingly, there was an improvement in the breadth of the components of the index, with seven of the 10 components making positive contributions.

Additionally, the rolling six- and 12-month rates of change appear to have bottomed out and should move higher in the coming months.

■ Previous Month ■ Current Month

Monetary Policy

What we see

Monetary policy is one of two ways the government can influence the economy and financial markets. By manipulating interest rates, the Federal Reserve can raise or lower the cost of money to stabilize or stimulate the economy.

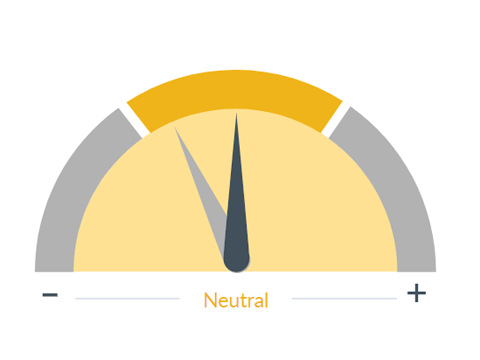

Dial 3: Monetary Policy 1:45— We also moved our Monetary Policy dial to the right. It is still in the yellow zone because the battle against inflation isn’t over, as we’ve seen with recent reports.

In the near term, while goods inflation may start to pick up and events in the Middle East remind us that we could see higher energy prices going forward, modest downticks in levels of sticky inflation, which we’ve seen recently, are encouraging and support our downward glide path for inflation viewpoint, which should, in turn, support our view of two to three rate cuts by the Fed [Federal Reserve] as it begins the process of normalizing monetary policy.

■ Previous Month ■ Current Month

Housing / Mortgages

What we see

Housing is an important indicator of the overall economy and a key driver of investment and job growth. We look at such things as starts, permits, foreclosures, delinquencies, and bank lending to assess the sector's health.

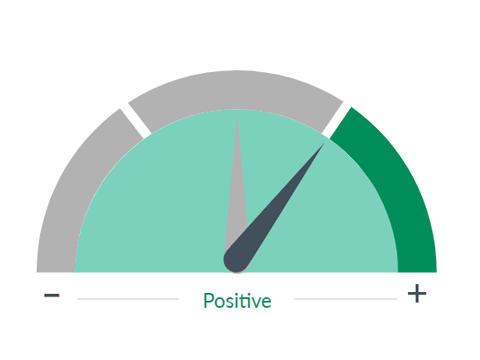

Dial 4: Housing / Mortgage 2:23— Housing should benefit from lower rates in the next six to nine months, so we shifted that dial into the green zone.

As we see it, there is pent-up demand for housing, and with interest rates expected to stabilize and move lower, mortgage rates should also turn lower. This should lower the affordability headwinds for many would-be buyers, leading to an improvement in housing permits and starts — which would be a boost to the economy overall.

■ Previous Month ■ Current Month

Credit Demand / Availability

What we see

Availability of credit from banks and the overall financial sector to provide capital to the economy. Restrictive credit conditions are a headwind to economic activity, while accommodating conditions may boost it.

Dial 5: Credit Demand / Availability 2:51— Relatedly, we have shifted our Credit Supply Demand dial into the green zone.

While overall demand for loans continues to slow, with interest rates expected to decline modestly, the improvements we’ve seen in recent surveys, such as the Senior Loan Officer Opinion Survey and the American Bankers Association Credit Conditions Index, should continue in the coming months, creating a more favorable environment for credit, removing a potential negative for the economy and, in turn, adding more capital to rebuild inventories and other working capital needs to grow the U.S. economy.

■ Previous Month ■ Current Month

Corporate Profit Growth

What we see

Corporate earnings have a significant influence on the stock market as they ultimately drive stock prices. The value of securities is the present value of all future cash flows.

Dial 6: Corporate Profit Growth 3:29— The final adjustment we’re making is to the Corporate Profit dial. While margins for corporations are elevated, the combination of higher GDP and moderating pressure on inflation and labor costs should result in Earnings per Share (EPS) growth for the S&P in 2024 at the upper end of our original forecast, so now we’re looking at a 9%-12% growth in earnings for the S&P 500.

In conclusion, our confidence in a soft landing for the U.S. economy continues to increase, supporting improvements in many of our dials.