Rochdale Speedometers: May 2026

This year has been anything but predictable. A volatile first quarter gave way to a surprisingly stable spring, and now, as we move deeper into the second half of 2025, the markets are once again at a crossroads. Tariffs have surged to their highest levels in over a century, yet inflation remains contained so far. Growth has cooled, but it hasn't collapsed and the labor market is softening but still generating jobs, despite the most recent revisions we've seen to start the month. And against that backdrop of mixed signals, equity markets have climbed back to all-time highs. For investors, the key question now is whether this stability is built to last, or whether we're merely in a lull before the next wave of volatility.

The answer, as always, lies in the underlying fundamentals. And this month, our Speedometer framework reflects a modest but meaningful shift. While we remain cautious in the near term, we're beginning to see areas of improvement as we peek into 2026 across three key areas: Consumer and business sentiment, growth and interest rates. This month's update incorporates those changes and takes stock of where we are in the cycle as we look toward the final stretch of the year. Ultimately, we see a domestic backdrop that remains uneven, but in some respects is on firmer footing than it was just a few months ago.

■ Previous Month ■ Current Month

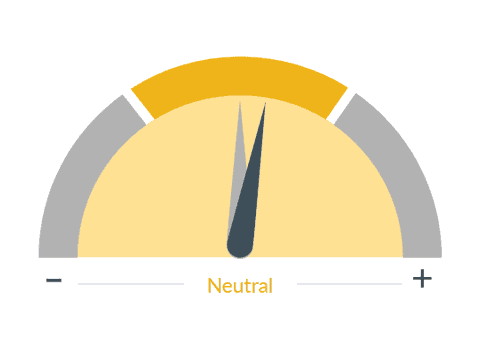

Consumer Sentiment

What we see

How consumers feel about their overall financial health as well as that of the economy on the short and long term. This is an important indicator, as the consumer is the largest driver of the U.S. economy.

Dial 1: Consumer Sentiment, 1:25— So, let's walk through these details. We've raised our Consumer Sentiment dial — still within the yellow zone, but no longer at neutral. This change reflects our view that while near-term risks to sentiment do remain elevated, the longer-term trajectory is improving.

Earlier this year, sentiment was hit hard by the magnitude of tariff announcements and the potential for increased inflation. These concerns, especially around consumer purchasing power, are still valid. We've seen renewed upward pressure on goods prices and a modest pullback in discretionary spending. The latest employment report also points to softening labor conditions, including a slight increase in the unemployment rate and substantial downward revisions to prior job gains. But looking ahead six to nine months, we see reasons for cautious optimism. Wage growth remains positive, and household balance sheets are generally healthy.

As the inflationary impact of tariffs gradually subsides we expect consumers to regain confidence. Importantly, markets are forward looking and while goods prices are higher, they've not surged to levels that threaten purchasing power. All of this leads us to believe that by the second quarter of 2026, consumer sentiment will be on a more constructive path, particularly if the labor market stabilizes.

■ Previous Month ■ Current Month

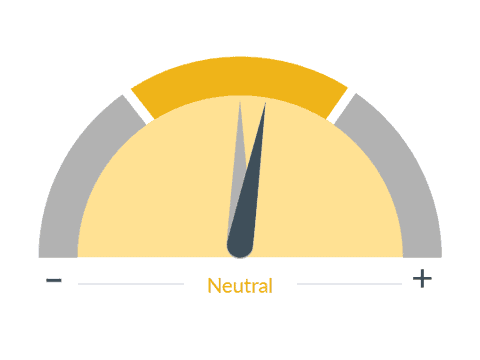

US Economic Outlook

What we see

City National Rochdale's investment and portfolio strategy is driven by our macroeconomic analysis. Timely economic forecasting is very difficult to do but extremely important, especially as the significance of economic information to financial markets continues to rise. To form a reliable outlook for the economy, City National Rochdale utilizes a comprehensive internal research effort that is complemented by an extensive set of external research from some of Wall Street's leading strategists.

Dial 2: US Economic Outlook, 2:38— Our second dial change the U.S. Economic Outlook, which is also being upgraded, remaining in the yellow but leaning more positive now. Economic growth remains modest, but several recent developments suggest a more durable expansion than we anticipated earlier in the year. GDP is tracking just above 1%, which is below potential but it is better than many feared following the initial tariff shock.

Business investment has held up, and corporate earnings continue to exceed expectations. That said, this is not a breakout moment for the economy. Productivity does remain weak, housing affordability continues to weigh on residential investment and the labor market has lost some momentum. But on the margins, the US economy continues to grow. Combined with improvements in consumer sentiment and signs of coming policy support, in the medium term, the balance of risks is shifting incrementally to the upside.

■ Previous Month ■ Current Month

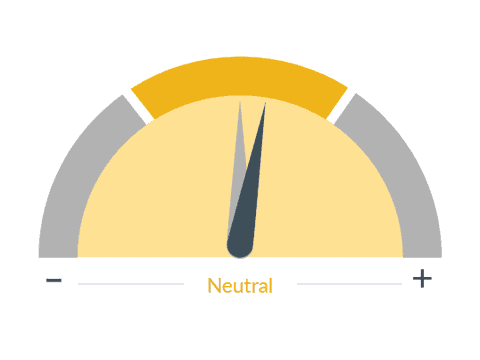

Interest Rates

What we see

Interest rates control the flow of money in the economy. High interest rates curb inflation, but also slow down the economy. Low interest rates stimulate the economy, but could lead to inflation. Interest rates affect the economy slowly. When the Federal Reserve changes the Fed Funds rate, it can take 12-18 months for the effect of the change to percolate throughout the entire economy.

Dial 3: Interest Rates, 3:29— Our third dial adjustment reflects a shift in the Interest Rate outlook. We're upgrading this dial to acknowledge growing evidence that yields may finally begin to drift lower. The Federal Reserve has not resumed rate cuts yet, but forward-looking indicators — slowing growth, moderating inflation and a softening labor market — suggest that policy easing is increasingly likely before year-end.

In recent weeks, inflation data has not come in as high as expected. Meanwhile, long-term inflation expectations have remained stable, even as short-term expectations have nudged higher due to tariffs. Combined with growing slack in the labor market, we believe the Fed will have sufficient justification to use policy, particularly if disinflation reemerges and unemployment trends higher. In that context, we now see a greater probability that the 10-year Treasury yield could fall below 4% and remain there sustainably into 2026.

This would mark a shift in the rate environment and could have broad implications for portfolio positioning, particularly in fixed income and duration-sensitive assets. As we look toward the second half of the year, our overall posture is more cautious but not bearish. Markets have climbed a wall of worry, but valuations are stretched. The S&P 500 is trading at 25 times earnings, levels rarely sustained without strong growth or substantial shift in monetary policy.

At the same time, volatility has begun to reemerge after a period of extreme calm. Investors are now reassessing risks around tariffs, Fed policy, geopolitical tensions and a cooling labor market. We believe now is a good time to take stock of our position. While we still see long-term opportunity in areas tied to innovation and infrastructure, particularly AI-driven capital investment, we are concerned about stretch valuations.

That leads us to believe the current environment calls for balance. And while the long-term bull case remains intact, near-term risks warrant caution.

So to summarize, we've upgraded three Speedometers this month: Consumer Sentiment, the US Economic Outlook, and Interest Rates. These changes reflect a cautious but constructive shift in the macro-landscape while growth is still below trend and risks remain.

The direction of travel is improving given rich valuations and the potential for volatility. We are considering a return to neutral equity positioning while remaining active and selective across asset classes. We believe this is a time for thoughtful diversification, risk awareness and staying focused on long-term fundamentals.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

CNR Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect City National Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

City National Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and City National Rochdale are subsidiaries of Royal Bank of Canada.

©2025 City National Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE