Economic Perspectives: Domestic Manufacturing: Making a Comeback?

The key takeaway this month is that while we have made several modestly positive adjustments to our dials to reflect the recent changes we've made to our GDP forecast, there are no changes to our higher-for-longer investment thesis, our expectations for a mild recession, or our moderately defensive portfolio position.

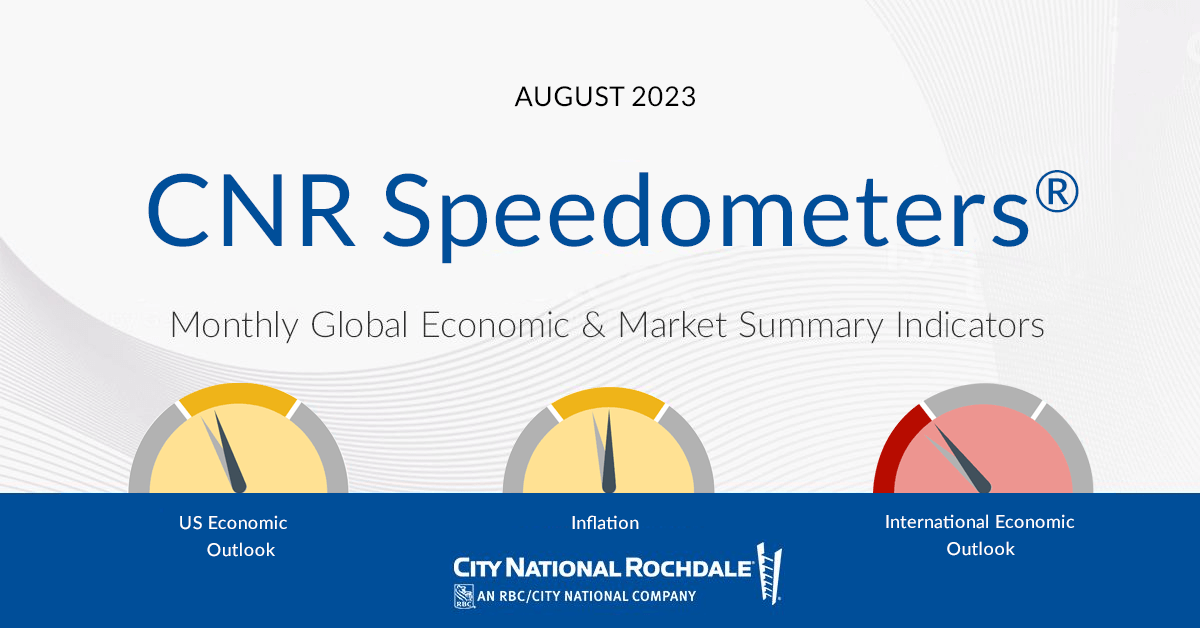

[ First Dial Update: 0:35 ] Let's dive into the changes in the dial, starting with Inflation. Recent reports have been encouraging. The headline CPI recently fell to 3%, while the core measure fell to 4.8%.

These reports support our expectations for a downward glide path in inflation over the next six to nine months in both the headline and core measures of inflation.

Remember from our recent comments that there's both good news and bad news on the inflation front. The good news is that the headline inflation is coming down and the pressures consumers have been facing for some time have fallen below the growth in wages. That's good news for consumer spending through the year end, and supports our mild recession expectation.

The bad news is that the core levels of inflation are stickier and higher than the Fed would like. That body’s focus on core inflation is the foundation of our higher-for-longer thesis. Net-net, there’s been a modestly positive tweak to the inflation dials — appropriate in our view — and inflation remains in the yellow zone.

[ Second Dial Update: 1:40 ] We've modestly increased the US Economic Outlook dial to reflect the recent increases we've made to our GDP forecast over the last month or so for 2023, with a shift to the right for the expected timing of a mild recession, which now gives us 74% probability (down from 78%).

The shift is based on the continued strength in the labor markets that we're seeing; the positive wealth effect of a solid price appreciation in both the stock market and the housing sector; and excess cash that's still in the system.

[ Third Dial Update: 2:16 ] We are also modestly tweaking the (International) Global Economic dial to the right to reflect the increase in U.S. economic activity, but keeping it in the red zone. We are still seeing sluggish economic activity in Europe and Japan, as evidenced by the recent PMI data, and we do not anticipate this situation will meaningfully improve through the next six to nine months. We continue to be skeptical on the rebound in China's economic activity, as global trade remains sluggish and job creation in that country is facing headwinds due to corporations seeking alternative supply sources in other countries. While we don't have any changes this month for our Corporate Profitability dial, I thought that since it’s earning season, I'd pass along a few key takeaways.

[ Dial Acknowledgements: 2:55 ] Firstly, revenue growth has been sluggish — basically flat, in fact. Margins are down 8%, and earnings are down about 7% so far. Secondly, there's been little change in the bottom-up estimates, and we remain below consensus (although that gap has narrowed meaningfully as the consensus has come down closer to our forecast). Finally, while overall results have been okay in comparison to consensus estimates, we're seeing greater divergence in results. Bigger companies are doing better than smaller companies, and the management tone is a bit more cautious. Given this backdrop, we're keeping our (Equity Market) Valuation dial in the red zone and feel comfortable with our modest underweight.

[ Summary: 3:45 ] In conclusion, we have made several positive adjustments to our dials this month to reflect recent changes to our GDP forecast. There are no changes in our higher-for-longer investment thesis, our expectations for a mild recession, or our moderately defensive portfolio position.