Rochdale SpeedometersSM

February 2026

Forward-Looking Six to Nine Months

TRANSCRIPT

This month, markets maintained their composure during major geopolitical events, including Venezuela, Greenland and the current situation with Iran. Gold and other metals experienced a major rally followed by a sharp correction. Equity markets rebounded from an intramonth decline and ended the month up about 1.5%. Put simply, it was a wild month.

Now to address it up front, let’s talk about gold. Prices have accelerated at an exponential rate. Since, 1996 the S&P 500 rose about 1500%, vs. gold up around 1250% through the end of last week. Prior to 2025, gold returned roughly 615% as the S&P 500 was up 1225% — a ratio of 2:1. Our feeling here is that gold is rising for the wrong reasons. It typically moves on lower interest rates and higher inflation — not the scenario we have today. The only explanation is that gold is a fear trade and we’re not fearful. While policy uncertainty can create some uneasiness, we see an underlying economy that is showing signs of growth, not contraction. While gold can add diversification to a portfolio, it is clearly disconnected from the fundamentals and its rise is unsustainable. We are not buyers of gold at these prices.

Moving into the economy, there was no shortage of media headlines in January, but the U.S. economy continues to grow faster than expectations. Third-quarter GDP came in stronger than expected on the back of continued consumer spending, which added 2.7% to GDP. The data tells us that we may have bottomed out in 2025 and that growth could be much stronger than expected in 2026. Linking the third quarter to the fourth quarter, economic data points continue to show a stronger Q4 than many economists projected given the likely drag from the government shutdown. Speaking of the shutdown late last year, Congress remains in a fight over the continuing resolution and funding bills, recently passing a bill to keep the government open, but the focus has shifted to funding for the Department of Homeland Security, which will now cease being funded on February 13th. We continue to expect noise here, but neither party wants a repeat of last year. We do see a path through.

One of the areas of concern has been the jobs market and we are still in the “no hire, no fire” environment. Fed Chair Jerome Powell noted in his remarks that there are some signs that the labor environment is starting to improve, but warned that there are still visible signs of weakness, largely offset by productivity gains the economy is experiencing from the deployment of AI. The December unemployment rate declined from 4.5% to 4.4%, while initial and continuing claims continue to trend lower — that’s a good sign and a leading indicator that unemployment isn’t set to rise dramatically.

What continues to be left out of the broader narrative is wage growth. Despite the affordability debate, lower-income consumers have seen their wages grow at the fastest pace relative to high earners and their net worths have nearly doubled. Private wages continue to grow, coming in at 3.8% since last year, but looking under the hood, non-supervisory workers, which make up about 80% of private payrolls, slowed to 3.6% from 3.8% the previous month. While slowing, these wage gains provide absorption for the increase in costs. It’s not 1:1, but we can’t focus solely on inflation when wages across all income groups are growing.

Where we remain concerned is on the housing market. Recent housing data points to continued demand in the face of very low supply. Housing simply isn’t affordable and that creates headwinds for spending… eventually. But most homeowners still have low rates, so the impact here is slow moving. While the market does remain slow, housing permits are ahead of estimates. We’ve also seen a pickup in refinance applications over the past few months as rates have come down slightly and we do expect the administration to be focused on bringing housing costs down, demonstrated by the potential for “Trump homes” to be built across the country. This has the potential to help but is not likely to come into play for at least a year.

Speaking of interest rates, the Federal Reserve’s independence was once again front and center in January. The Supreme Court has kept Fed Governor Lisa Cook on the Fed for now and comments from the justices point to a reluctance to allow the president to fire her. So far, this is a net positive for Fed independence. And while that decision remains ahead of us, the FOMC decided to leave rates unchanged in January, noting that labor is showing some signs of relief as the economy continues to grow at a solid pace. President Trump has also announced his nomination for the new chair of the Federal Reserve: Kevin Warsh. He will still need to be confirmed by the Senate, which we see as likely, but may be held up due to the ongoing investigation into building improvements at the Fed. Warsh is a good choice and a win in our opinion. While he is still a partisan pick, he has experience on the Fed through crisis and is likely not as dovish as the president would have preferred. The move so far is viewed by members of Congress and the markets as supportive of the Fed’s independence. Of course, his success will be based on building consensus amongst the Fed governors and he will need to demonstrate a steady hand with rates, instead of simply slashing them once at the Fed.

Before turning to this month’s Speedometers, I want to point out that we are in the middle of fourth quarter earnings season. We are seeing earnings advance again beyond expectations. And the moves we are seeing in tech don’t line up with the fundamentals. On average, tech names are beating expectations by 8%, above the broader markets’ beat rate of 2%. We expect this to level out some of the decline in tech names we’ve seen so far this year. Now let’s turn to our estimates: We’ve raised our U.S. GDP growth estimates for 2026 to between 2% and 2.5%, but we did make some downward adjustments to our Speedometers by lowering Consumer Sentiment and Fiscal Policy.

■ Previous Month ■ Current Month

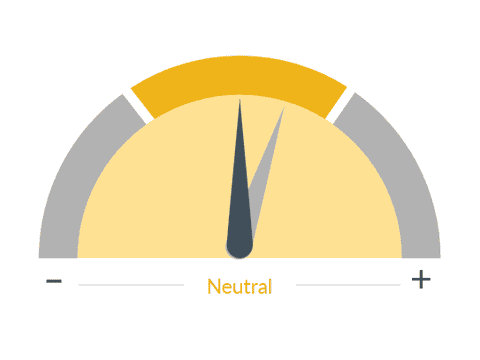

Consumer Sentiment

What we see

How consumers feel about their overall financial health as well as that of the economy on the short and long term. This is an important indicator, as the consumer is the largest driver of the U.S. economy.

Dial 1: Consumer Sentiment, 6:08— While consumer spending remains strong, consumer sentiment has been at a low for years and has clearly been neutral in terms of its impact on markets. We view sentiment as primarily policy-related, not a reflection of the underlying economy. While sentiment may be low, it hasn’t stopped spending.

■ Previous Month ■ Current Month

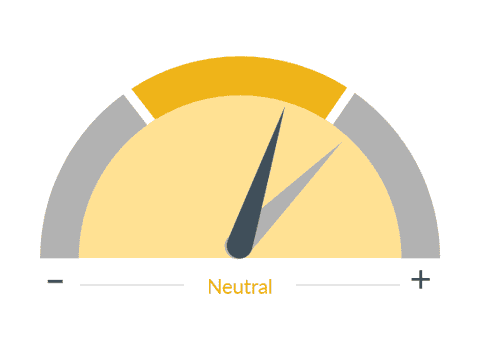

Fiscal Policy

What we see

Changes in tax rates, regulations and government spending affect the decision-making process of consumers and businesses. By changing tax laws, the government can effectively modify the amount of disposable income available to taxpayers or raise the costs for businesses.

Dial 2: Fiscal Policy, 6:30— We also lowered fiscal spending from green to yellow, reflecting a front-loaded fiscal situation from tax refunds, but there is potential for spending to slow later this year. We’re also a little concerned about some of the recent announcements, like capping interest rates on credit cards at 10%, which could impact access to credit.

While we see the administration’s efforts to deregulate as a net positive, actual spending is likely to slow — that’s not a bad thing, but certainly won’t drive the market. For now, we see the economy accelerating and view the current pullback in tech as a net positive to shake out a little bit of the valuation premium.

Important Information

RBC Rochdale, LLC. is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

Rochdale Speedometers are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect RBC Rochdale’s overall outlook of the economy.

RBC Rochdale, LLC., its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

©2026 RBC Rochdale, LLC. All rights reserved.