-

Market Perspectives

Be Still My Beating Heart

February 2026

- Filename

- Market Perspectives February 2026.pdf

- Format

- application/pdf

.jpg "Charles Boettcher, CPWA®")

TRANSCRIPT

The S&P 500 was up 1.45% in January, a good start to the year; however, February has been a bit volatile so far, making our hearts flutter and not for the traditional February reasons. The first few trading days of the month pushed the year-to-date return slightly into negative territory. A recent rebound has pushed it back into positive territory. It’s a reminder that short-term volatility can manifest at any time, for many reasons, especially when equity valuations are rich. The catalyst for the recent volatility? Largely, it was potential AI-related disruption to the software and software as a service industries.

On Friday, January 30th, Anthropic’s Claude Cowork launched, contributing to previously declining industry performance. Eleven open-sourced plugins covering sales, marketing, finance, legal, research, and more brought threats to existing integrated software firms. The concern is AI agents could directly replace software workflows. Some software names, many being last year’s darlings, oversold, in our opinion. A positive is the valuations for said stocks corrected to attractive levels, with some price-to-earnings ratios hitting 10-year lows. More analysis is needed to determine true lasting impacts. Anyway, it’s a reminder that the AI impact is real, but still early.

Let’s spend some time on the characteristics of the S&P 500 behavior in 2026. So far, value has outperformed growth, low quality has outperformed high quality, and high beta has outperformed low beta. Will this persist?

High beta could possibly continue to lead. High beta stocks lead the recovery from the April tariff crisis lows. If so, more defensive portfolios may lag. Further, rate cut expectations favor higher-risk assets.

Regarding low vs. high quality, we have high confidence these will reverse; quality positioning is expected to recover as speculative trends exhaust. Companies with weaker earnings quality generally underperform in the long run.

Finally, there's value versus growth. Heading into this year, the valuation gap was wide between growth and value stocks. Value may likely outperform intermittently when volatility spikes, AI enthusiasm wanes, or simply because of some good old-fashioned profit taking. Looking beyond the moment, growth and AI stocks are likely to have a structural earnings advantage.

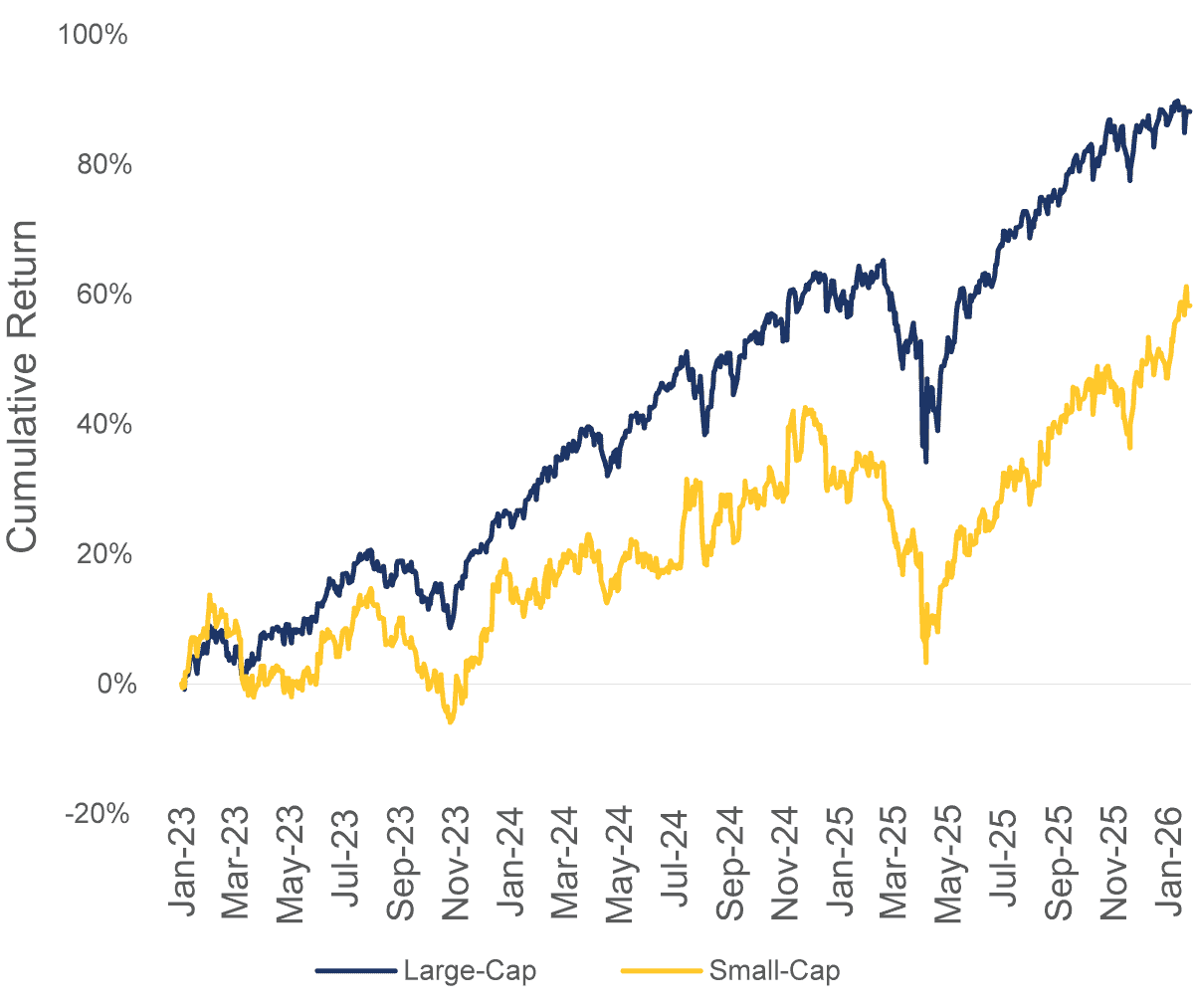

Large & Small-Cap at All Time Highs

The Good News:

- Wall Street Consensus S&P 500 target: 7,400-7,500 (+8.1% upside)

- RBC Rochdale target: 7,700-7,800 (+12.1% upside)

- Expected 13.5% EPS growth ($269.28 $305.70)

- AI capex cycle continues ($500-600B projected in 2026)

The Challenge:

- Forward P/E: 25.7x (avg since 2012 = 19.1x)

- Returns must come from earnings and not valuation expansion

Source: Bloomberg, RBC Rochdale. As of 1/27/2026. Large Cap – S&P 500 Index. Small-Cap – Russell 2000 Index.

Information is subject to change and is not a guarantee of future results.

Chart 1, 2:54— And speaking of earnings, one of our favorite topics, earnings-per-share growth this year is expected to reach double digits. Such expectations drive S&P 500 return estimates: Wall Street is targeting a year-end S&P 500 between 7,400–7,500. We at RBC Rochdale are a bit more optimistic, with a target in the 7,700–7,800 range.

The challenge, as you have heard us say many times, is the current valuation. We feel strongly that returns this year must come from earnings growth, as there is not much, if any, room for multiple expansion.

We are early in the fourth guarter earnings reporting season, but we are off to a good start. Approximately 14% of S&P 500 companies have reported Q4 earnings, and about 77% have beat earnings expectations. I plan to dive deeper next month after more companies have reported.

To sum up: Markets anticipate high-single to low-double-digit equity returns in 2026, driven by low-double-digit earnings growth. Early 2026 has seen a “lower quality rally.” Higher-quality stocks are expected to outperform for most of the year, though quality market-sensitive stocks may still lead. Technology capital expenditures (CapEx) are accelerating, with benefits expected to expand to AI adopters and beneficiaries beyond hyperscalers. Q4 2025 earnings so far have slightly exceeded expectations and long-term averages, though the season is still early.

Important Information

The views expressed represent the opinions of RBC Rochdale, LLC which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness.

While RBC Rochdale believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and management's view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market.

Equity investing strategies & products. There are inherent risks with equity investing. These risks include, but are not limited to stock market, manager or investment style. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices.

RBC Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

Index Definitions

The Standard & Poor’s 500 Index (S&P 500) is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity and industry group representation to represent U.S. equity performance.

The index represents large-cap stocks, generally defined as companies with market capitalizations over $10 billion. Small-cap stocks are generally defined as companies with a market capitalization between $300 million and $2 billion.