Market Perspectives: May the Stocks Be With You

The key takeaway this month is that while we have one modestly negative and three modestly positive adjustments to our dials, recent events and the latest economic report support our expectations for a mild recession, the timing of which continues to remain elusive.

Let's start with the three recent economic updates: First, while Q2 GDP activity was revised modestly higher, driven by increased personal consumption and a better balance of trade, this momentum may slow in coming months. The balance of trade data historically has been very volatile and can quickly shift and become a negative headwind. Second, while personal consumption growth has been strong because of the tight job market, consumer spending has slowed, likely reflecting lower cash reserves and tighter lending conditions. These headwinds to the consumer should continue in coming months at a time that the resumption of college loan payments for many will likely lead to modestly lower spendin,g starting in the fourth quarter. Lastly, while durable goods orders did tick up recently, the ISM manufacturing indices continue to move lower, indicating the recent demand for equipment could slow in coming months. We believe that these recent economic data reports are already reflected in our Speedometers.

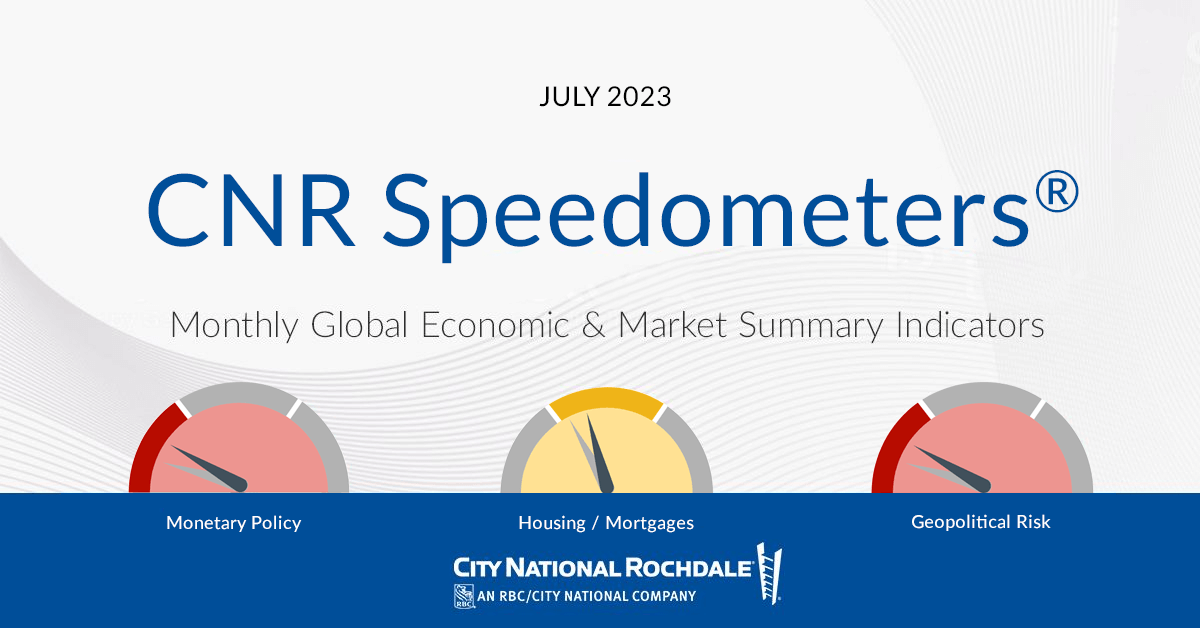

[ First Dial Update: 1:45] The first change in our dials is the housing dial, which we are moving modestly to the right. Despite higher mortgage rates from a year ago, the housing market continues to show signs of stabilization. Inventories remain tight, and housing starts as well as builder sentiment have both improved. However, we remain watchful on housing over the next few quarters, as lending conditions continue to tighten and affordability remains low, so this month it's just a modest shift to the dial, which remains yellow.

[ Second Dial Update: 2:15 ] The second modestly positive shift we're making is in the monetary policy dial, as we believe we are coming closer to the end of the Fed's hiking cycle. It's important to note that we are keeping the dial in the red zone as the Fed will need to keep rates higher for longer to cool upward pressures that exist in wages and core levels of inflation.

[ Third Dial Update: 2:36 ] The last modestly positive shift in our dials is on the geopolitical front. While risks from exogenous shocks remain at the top of the things that keep me awake at night, and the dial remains red, we are encouraged that the U.S. and China are continuing to have dialogue about lowering tensions. And with the recent developments in Russia, who knows? Maybe it could make China rethink it's strategic commitment to its volatile partner.

[ Fourth Dial Update: 3:01 ] The final change in our dials relates to equity valuation. We've lowered the equity valuation dial into the red zone, as we indicated at last month's webinar. There are two reasons for this: First, because earnings estimates have gone down, as stock prices have gone up, the price earnings multiple for stocks has increased over nineteen times forward earnings. Second, with stocks becoming more expensive, the relative appeal to fixed income also shows the equity risk premium has gone down.

[Summary: 3:33 ] In conclusion, while we have one modestly negative and three modestly positive adjustments to our speedometers this month, recent events and economic reports support our expectations for a mild recession, the timing of which continues to remain elusive.