Rochdale Speedometers: May 2026

There was very little change in our Speedometers® this month, but the majority of the April data releases helped to confirm our opinion of the current outlook. The key takeaway today is that the economy remains strong, despite the estimate for GDP in the first quarter coming in below expectations.

The economy advanced at a 1.6% pace, and that’s below the median forecast of 2.5% and 3.4% for the prior quarter. But this was largely due to a contraction in company inventories and a large negative contribution from foreign trade.

■ Previous Month ■ Current Month

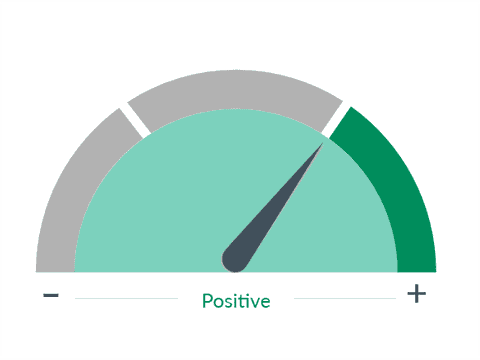

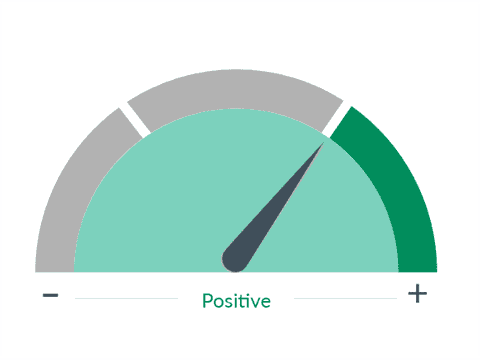

Housing / Mortgages

What we see

Housing is an important indicator of the overall economy and a key driver of investment and job growth. We look at such things as starts, permits, foreclosures, delinquencies, and bank lending to assess the sector's health.

Dial 1: Housing/Mortgages 0:46— Notably, the economy did experience a double-digit pace of growth in housing (13.9%) and continued growth in consumption (about 2.5%). Excluding the impact of inventories and trade, the economy grew closer to 3% in Q1. The GDP report had the largest positive impact on our Housing Speedometer®, which we had recently taken into the green. Other positive contributions to our outlook from the release confirmed our levels on the U.S. economic outlook and consumer spending with tangential effects on corporate profit growth and disposable personal income.

A big data point in April was the beginning of earnings season, and that arrived in full force on April 26. Over 150 companies reported earnings, including some of the biggest tech names in the S&P 500 such as Tesla, Meta, Microsoft, and Google. At the conclusion of the week, about 42% of the market had reported, and 82% of those names beat expectations by an average margin of about 10%.

Some concern was hanging over the market just based on high expectations, but so far, companies have delivered. And given the continued strength in equities, we do believe that market valuations are on the high end, and our Speedometer® will remain in the red for now. But the strength in earnings confirms our outlook for corporate profit growth, and we are maintaining our 9% –12% target for full year 2024 earnings.

■ Previous Month ■ Current Month

Inflation

What we see

While a slow, persistent rise in prices is consistent with a healthy, growing economy, a rapid increase in inflation, especially if unanticipated, can be harmful. Inflation means higher consumer prices, which often slows sales and reduces profits.

Dial 2: Inflation 2:09— Inflation Now, let’s turn our attention to price levels and our Inflation Speedometer®. A concern in April was data indicating an advance in inflation expectations, and that came in well above what the market was expecting. We had recently upgraded our inflation dial to green entering 2024 by taking stock of the consistent decline from levels that were above 9% in 2022 to below 4% today.

Looking back, it would be easy to say that that shift was a bit premature, but we don’t see enough evidence yet to move in the opposite direction.

The outlook for a soft landing has improved, and trends within the economy point to a sustained path lower but potentially more gradual course on inflation. Combined with our geopolitical concerns and the U.S. elections later this year, we are going to stay put in our view that inflation will resume its decline.

■ Previous Month ■ Current Month

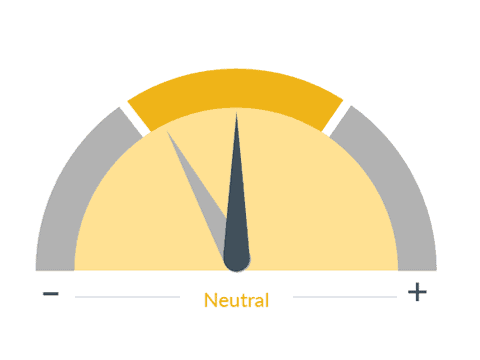

International Economic Outlook

What we see

The world has become increasingly interconnected through trade and the flow of capital, and emerging markets in particular have risen in importance as drivers of global growth. Moreover, we believe a global perspective is integral to any investment strategy.

Dial 3: International Economic Outlook 2:58— The one change we made to our Speedometers® this month was a positive one, with the International Economic Outlook dial moving to a neutral position.

Recent business activity survey data has been supportive of a pickup in global business activity. The International Monetary Fund (IMF) has echoed this assessment in their latest World Economic Outlook report.

They increased their forecast for 2024 global GDP by .1% to about 3.2%, which is the same run rate as last year. That is an improvement, but a large proportion is being driven by better U.S. prospects. We’re still neutral because global growth is expected to remain below the historical level of about 3.8%. But continued progress on inflation and a conclusion to the global central bank rate hiking cycle has the global economy setting up for another year of steady growth.

Much of what we see as a headwind to the market, and the position of our dials, is coming from the stance of the Federal Reserve, the overall interest rate picture, and the ever-present overhang of geopolitical risk.

However, it is looking increasingly likely that over 2024, earnings will continue to be key, and they do have the power to overcome challenges from inflation and high interest rates.