Rochdale Speedometers®

October 2025

Forward-Looking Six to Nine Months

TRANSCRIPT

Over September, markets staged another rally, capped by a rare quartet of highs across the S&P 500, the Russell 2000, the Nasdaq 100, and the Dow Jones Industrial Average. It’s not often that all four of these indexes set records together, and when they do it usually signals breadth in the rally and confidence in the economic outlook. Gains are being driven by both large cap leaders and small caps, with strong earnings momentum, lower rates and steady growth all supporting equity markets.

Despite the new all-time highs, we’ve kicked October off with a government shutdown, and while we are concerned about the potential longevity of the standoff, our research shows that shutdowns rarely create equity losses. Going back to 1981, stocks averaged a 3.1% gain one month after the closure and 11.4% after 6 months. We’re hopeful for a resolution soon, but we do not believe the market impact will be significant.

For a detailed breakdown of the government shutdown announcement and what it means for your portfolio, check out our latest special bulletin article.

> Government Shutdown: What It Means for Markets

Back to the data, retail sales came in well ahead of expectations, underscoring the strength of consumer demand. There are certainly headwinds for some households, especially those more heavily impacted by higher prices and recent cuts to benefits. But nearly all groups stand to benefit from fiscal stimulus measures that will go into effect in the months ahead. Many continue to underestimate the impact of the administration’s fiscal spending bill, which provides significant tax relief and sets up the potential for substantial refunds early in 2026. Combined with elevated wages and lower interest rates, these measures are laying a strong foundation for continued spending.

On the labor side, conditions are softening but the picture is complicated. Job growth has slipped below breakeven, initial claims are at their highest since late 2021 and youth unemployment has been rising. Some of this may be due to the AI transition, but the bigger issue is that there are fewer entry-level job openings because of very low churn in the labor market. Firms are reluctant to hire, but they are also reluctant to fire, which leaves younger workers facing limited opportunities. Meanwhile, government layoffs tied to budget constraints and weaker immigration flows are adding to the distortions. The result is a labor market that feels weaker, even if it isn’t collapsing.

The Federal Reserve has responded to these risks. After cutting rates in September, officials have signaled more easing is ahead of us. Chair Powell has emphasized that tariff-driven inflation is likely to be a one-time adjustment, not a long-term problem, and that employment is now the greater concern. Importantly, Fed independence has been under scrutiny. The administration has challenged Governor Lisa Cook and elevated Stephen Miran, who dissented at the last meeting. But Miran was the lone dissenter, and the broader committee showed unity in moving policy forward. That gives us hope the FOMC is committed to its dual mandate of stable prices and maximum employment, even under political pressure. A reassuring sign for markets.

Turning to housing and inflation, conditions are beginning to change. Housing makes up nearly 40% of CPI and has been offsetting the increase in goods prices. But Fed rate cuts are already giving housing a boost. New home sales surged more than 20% in August, the strongest pace since early 2022, as lower mortgage rates drew buyers back. Mortgage applications also jumped sharply, signaling significant pent-up demand for refinancing that will be released as rates continue to fall. While this is a tailwind for spending, it also means the downward trend in housing prices could stabilize or even reverse, reducing the deflationary offset and keeping prices somewhat stickier than expected. That is a risk, but we are not talking about runaway inflation. If spending, investment, and policy follow-through stay on track, the economy should be able to weather it.

We are making a few changes to the Speedometers this month by upgrading Consumer Spending and Interest Rates.

■ Previous Month ■ Current Month

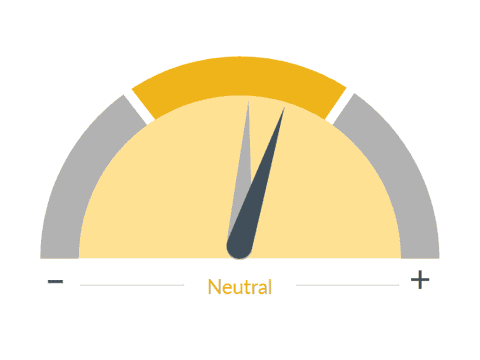

Consumer Spending

What we see

Aggregate level of consumer spending. Since consumers are the largest driver of the U.S. economy, their spending patterns have a large impact on overall economic activity.

Dial 1: Consumer Spending, 4:12— Consumer spending has held up better than expected, and we expect conditions to improve over the next six to nine months. The administration’s fiscal spending bill provides meaningful fiscal support, and together with elevated wages, this strengthens the outlook for both higher- and middle-income cohorts. While some households continue to struggle, particularly in the face of higher costs and reduced benefits, the top third of earners — who drive the bulk of spending — are increasingly confident in their future income prospects.

Retail sales came in well above expectations and consumer surveys show optimism is building as stimulus measures begin to take effect. Lower interest rates are another important factor, not only boosting mortgage applications but also lifting consumer sentiment more broadly. This combination of fiscal, wage, and policy tailwinds drives our decision to upgrade the Consumer Spending dial, while keeping it in the yellow zone as we watch how the benefits flow through.

■ Previous Month ■ Current Month

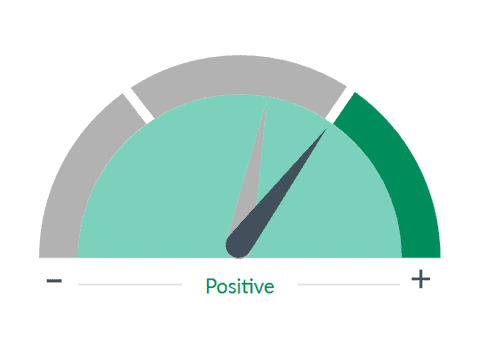

Interest Rates

What we see

Interest rates control the flow of money in the economy. High interest rates curb inflation, but also slow down the economy. Low interest rates stimulate the economy, but could lead to inflation.

Dial 2: Interest Rates, 5:07— Moving to interest rates. The Federal Reserve’s September cut marks the resumption of an easing cycle that we expect to continue into 2026. Powell and most of the committee made clear that they are prioritizing labor stability over near-term inflation worries.

The policy outlook is supportive across multiple channels. Lower rates are easing financial conditions, with equities making new highs and credit spreads tightening. As I noted earlier, Housing is responding quickly, with new home sales surging and refinancing activity set to accelerate. We also expect the yield curve to steepen modestly, with front-end yields falling faster than long-term rates, and the 10-year Treasury moving toward or below 4% over the next few quarters. This combination of clearer policy direction and constructive market response supports moving the interest rate dial to the green zone.

Outside of these changes, other indicators continue to show a mixed but steady picture. AI-driven capital spending remains a powerful force, offsetting weakness elsewhere and helping lift GDP to around a 2% pace this year and next. At the same time, geopolitical risks remain elevated, particularly around energy markets and the Ukraine conflict, which could add volatility. Fiscal uncertainty, including government shutdown risk, still lingers, though we expect these episodes to have only modest economic and market impact if they are short-lived.

Looking into 2026, we expect growth to run slightly above potential, with GDP expanding just over 2%. Inflation will remain under pressure but should end the year below 3%, allowing for about three additional Fed cuts. Corporate earnings are expected to remain stable despite some margin pressures, and long-term interest rates should drift modestly lower as easing continues.

As we look forward, we remain constructive on equities into year-end. But with valuations stretched in U.S. large caps, we see opportunity in small caps, which tend to outperform early in easing cycles. We also believe international equities may be nearing a critical turning point. A weakening U.S. dollar is typically a necessary condition for strong non-U.S. performance, and that condition is becoming more likely. If U.S. markets stumble — which is not our base case — dollar pressure will accelerate. This creates potential for strong returns abroad alongside diversification benefits.

For these reasons, we are actively considering adjustments in our allocation guidance to capture these opportunities and set portfolios up for a successful 2026.

Important Information

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

Rochdale Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect RBC Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

RBC Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and RBC Rochdale are subsidiaries of Royal Bank of Canada.

©2025 RBC Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE