Market Perspectives: May the Stocks Be With You

As we move into the final two months of 2025, the backdrop for investors is one defined by policy uncertainty but also by the economy’s impressive ability to adapt. Tariffs, fiscal negotiations and a prolonged government shutdown have all contributed to a noisy environment, but the U.S. economy has managed to keep its footing and push ahead.

The trends in inflation are encouraging. The annual pace has settled just above 3%, right within our expected range and the monthly data continues to show a clear, slowing trend. We still expect inflation to remain above 2%, but to gradually decline through 2026 as price pressures continue to normalize. That’s a welcome outcome given the uncertainty earlier this year when tariffs were introduced in March.

Interest rates have been stable, holding within our expected range of 3.75 to 4.25% and the broader economy remains on the right track. Corporate earnings season for the third quarter has been solid, with most companies reporting results that are in line or better than expected. This has given investors some much-needed reassurance in what’s been an uneasy environment.

Still, there are challenges worth watching. The government shutdown has now stretched into its fifth week, creating short-term disruptions in spending, contracting and data reporting. Further, the November state and local elections will be a focal point for investors seeking early insight into policy direction ahead of next year’s midterms. While no major surprises are anticipated, it underscores how political developments continue to shape the market environment.

For a detailed breakdown of the government shutdown announcement and what it means for your portfolio, check out our latest special bulletin article.

> Government Shutdown: What It Means for Markets

Even so, the bigger picture is one of progress. Inflation fears appear to be behind us, rates are stable, corporate results are holding up and the economy continues to expand — all while navigating an unusually complex policy landscape. And that balance is reflected in our Speedometers this month, where we’ve made two important upgrades to the Yield Curve and Energy Price dials, both moving into the green zone.

We’ll come back to those changes in a moment, but let’s start with the Federal Reserve and the broader policy backdrop.

At its October meeting, the Federal Reserve lowered the federal funds rate by another quarter point — bringing it to a range of 3.75 to 4%— and announced that its balance-sheet reduction will officially end in December, which is positive for market liquidity. During the press conference, Chair Powell struck a balanced tone. He made it clear that another cut in December isn’t guaranteed, but he also emphasized that the risks to employment are now front and center as the Fed considers its next steps.

That’s even harder to gauge when government data releases are delayed by the shutdown, leaving policymakers to rely on partial information. We don’t believe they are operating completely in the dark, but the Fed is navigating a delicate transition — continuing to ease policy gradually to make sure tight financial conditions don’t start doing more harm than good. That balance between fighting inflation and supporting the labor market will define monetary policy in the months ahead and it’s one of the key reasons markets still expect additional support next year.

And that brings us to the labor market itself. It has started to show more noticeable signs of cooling. Unemployment has moved a bit above 4% and while that’s still low by historical standards, the pace of hiring has slowed more than expected. Playing devil’s advocate to the weakness, there may be several factors behind this slowdown that reflect temporary adjustments rather than signs of real weakness in the private sector.

First, immigration has fallen sharply this year, which means fewer new workers are entering the labor force. Second, government hiring has slowed as federal spending and contract funding have been reduced. And third, we’ve seen business leaders become a little more cautious in their hiring plans, given uncertainty around tariffs, trade policy and the broader economic outlook.

Together, those trends have restrained job growth and forced unemployment to rise. While the uptick has been meaningful, it doesn’t necessarily signal a downturn — just a cooling period after years of unusually strong gains. But if unemployment continues to rise, it could tip the balance and weigh more heavily on growth and confidence.

That’s why the Fed’s next steps are so important — continued rate cuts and a more supportive policy stance can help stabilize the job market before weakness becomes self-reinforcing. For now, we’d describe the labor market as softening, not breaking — and there’s reason to believe the recent uptick in unemployment could prove temporary if policy remains flexible and inflation keeps trending lower.

While the job market has softened, corporate performance has remained a bright spot — offering a more encouraging picture of the overall economy. Businesses may be hiring more cautiously, but they’re still delivering strong results — finding ways to protect margins, manage costs and adapt to a shifting policy environment. Earnings season for the third quarter has made that clear.

Across the board, results have come in stronger than expected, with most S&P 500 companies beating both earnings and revenue estimates. About three-quarters of companies have reported and roughly 70%have topped consensus expectations on earnings per share — a pace that’s above the long-term average.

Technology once again led the way. The major cloud and AI platforms posted another round of solid growth, driven by enterprise spending and continued adoption of data infrastructure and AI applications. While margins have narrowed in some areas, operating efficiency and scale continue to support strong profitability across the tech sector. Large-cap tech earnings were particularly impressive, with the big three cloud providers reporting double-digit revenue gains and stable guidance heading into year-end.

Results have also been good outside of tech, proving that earnings growth is not limited to a single sector. Financials have reported earnings up roughly 8%year-over-year, supported by improved trading volumes, stable credit quality and firm capital markets activity. Industrial companies have delivered gains of around 6%, helped by steady demand in transportation, aerospace and manufacturing.

Even in consumer discretionary, where spending has cooled, profits have surprised to the upside — rising about 5% on stronger margins and cost discipline.

Together, these results helped stabilize sentiment after a volatile summer. Valuations remain elevated in parts of the market, but strong earnings continue to offset those concerns. And with inflation moderating and rates steady, investors appear more confident that corporate profits can grow at a sustainable pace into 2026.

Now let’s turn to the Speedometers and discuss our changes.

■ Previous Month ■ Current Month

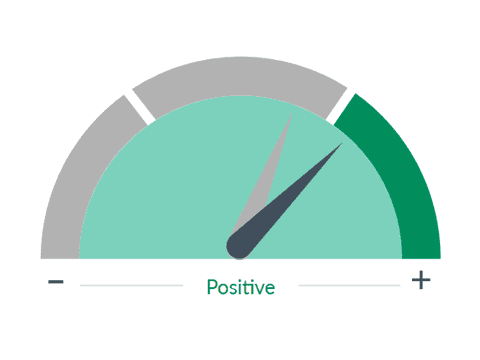

Yield Curve

What we see

The shape of the yield curve, which can be normal, inverted, or flat, provides insight into future interest rate changes and economic activity, with each shape signaling different economic trends, such as growth, recession, or transition.

Dial 1: Yield Curve, 6:52— The first change is the Yield Curve. For nearly two years, the curve was inverted — with short-term rates higher than long-term rates — often a warning sign of recession. But as the Fed has lowered short-term rates and inflation has come down, that inversion has finally corrected. The curve is now more normally shaped — a sign that the market sees a path toward continued growth rather than contraction.

That’s constructive for banks, for credit markets and for the broader economy. With additional Fed cuts likely in the coming months combined with our view of steady long-term rates, the curve should steepen further — a clear positive for the economy.

■ Previous Month ■ Current Month

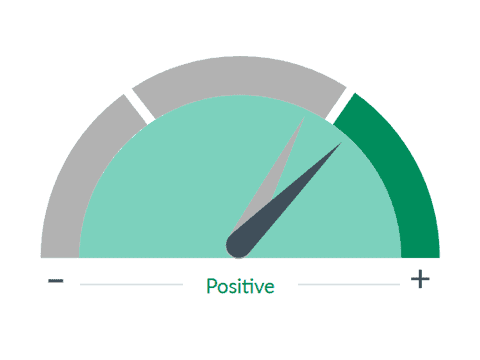

Energy Costs

What we see

Significant changes in energy/oil prices can have important but differing impacts on the overall economy. Higher energy prices act as a tax on consumers and businesses, absorbing money that would normally be used to buy other goods.

Dial 2: Energy Costs, 7:30— Our second upgrade is Energy Prices. Crude oil is trading near sixty dollars a barrel — well off its lows for the year. While OPEC has announced only a modest production increase for December and plans to pause in the first quarter of 2026, supply remains ample and while prices may fluctuate, we don’t see a risk of persistent price pressure. Prices could drift modestly higher if global activity picks up, but that’s not likely to put much pressure on consumer prices or spending.

History shows that energy prices become a real economic threat only when they rise sharply and stay high for an extended period — and that’s not the case today. At current levels, energy prices are helping the economy by keeping inflation pressures in check, lowering business costs and supporting household spending.

Looking ahead, the U.S. economy appears to be regaining its footing after a long period of adjustment. Inflation continues to trend lower, interest rates are stable and the yield curve has returned to a more normal shape. Corporate profits are improving and energy remains a modest tailwind rather than a risk.

That said, risks haven’t disappeared. The labor market still bears watching, fiscal uncertainty lingers and global trade policy remains unsettled. But overall, the environment is stable — supported by steady consumer spending, a healthy technology sector and the Federal Reserve’s gradual shift toward easier policy.

We also recognize that markets have moved quickly this year, particularly in the U.S., where equity valuations now sit above our long-term expectations. While recent earnings growth has been solid, it hasn’t fully explained the pace of this year’s market gains. That doesn’t mean the market is ripe for a sustained downtrend, but it does suggest that future returns may depend more on continued policy support and sustained corporate performance than on multiple expansion alone. The bottom line is that the margin for error has narrowed considerably.

By contrast, several international markets now offer historically attractive valuations relative to the U.S., with improving growth prospects and less policy friction. Positions in these markets could serve as a potential haven if U.S. equities face renewed pressure in the months ahead.

For now, our outlook remains cautiously optimistic. The economy continues to expand, inflation is moderating and financial conditions are improving — a combination that supports steady growth as we close out the year.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

Rochdale Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect RBC Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

RBC Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and RBC Rochdale are subsidiaries of Royal Bank of Canada.

©2025 RBC Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE