-

Fixed Income Perspectives

Income to Reward Investors

June 2024

- Filename

- Fixed Income Perspectives JUNE 2024.pdf

- Format

- application/pdf

Series Overview

Watch this new monthly video series featuring Director of Fixed Income, Micheal Talia, as he discusses trends within the macroeconomic landscape affecting Fixed Income markets and interest rates.

After 20+ years of zero interest rate policy, an entirely new set of opportunities is available to investors with higher yields and more dispersion, which have the potential to positively impact returns. Mike will help dismantle the complexity of bonds by exploring the differences between asset types and distilling the labyrinth of economic factors into what matters most for investors.

TRANSCRIPT

Since our last update, bond market volatility remains front and center, as Fed policy remains paused.

Moderating Economic Data Supports Bond Rally

Source: Bloomberg as of 6/5/2024, US Treasury yield curve. Information is subject to change and is not a guarantee of future results.

Charts 1 & 2: 0:22– As you can see with this chart of the 10-year Treasury, for much of the year, the bond market has experienced a bumpy path higher in yields, and this has been driven primarily by lingering inflation concerns, strong employment gains and a hawkish Fed. However, during May, Treasury yields declined, and this was driven in part by soft payroll data and consumer spending, while the CPI [consumer price index] signaled inflation pressure may be easing. While it’s notable that this decline in yields has continued through the first week of June, yields are still broadly higher across the curve from where we started the year.

And despite the volatility, we continue to believe the underlying economy remains in good shape and economic growth will continue to be driven by a more measured consumer as higher interest rates, slower job gains and depleted savings start to have an impact. As a result, we continue to forecast zero to two rate cuts from the Fed this year.

US Treasuries: Supply & Demand

Sources: Chart 3: Congressional Budget Office, Treasury Borrowing Advisory Committee, Securities Industry and Financial Markets Association. MetLife Investment Management. Chart 4: Bloomberg as of May 2024, Information is subject to change and is not a guarantee of future results.

Charts 3 & 4: 1:18– In our view, a more guarded Fed has been one factor contributing to U.S. Treasury yields remaining higher than where we began the year. And as we look out to the remainder of 2024 and into next year, we forecast 10-year yields to remain above 4% despite Fed easing. The charts above are one core reason why: on Chart 3, because of ongoing budget deficits, over $3 trillion in Treasury issuance is expected over the next five years.

Chart 4 shows how the buyer base of U.S. debt has been changing, as foreign holders have reduced exposure. While domestic buyers like households, banks and mutual funds have picked up the slack and now represent nearly 50%, the uptick in supply will lead to additional price sensitivity. Taken together, this supports an extended “higher-for-longer” theme and will continue to provide opportunities across markets.

So what does this mean for fixed income investors? Well, it’s hard to ignore yields that remain at decade highs, and with Fed policy approaching a turning point, the risk-reward trade-off from holding fixed income is well balanced. This means that for short-term cash investors with liquidity needs, short-term bonds remain attractive, with Treasury yields between 4.85% and 5.4%.

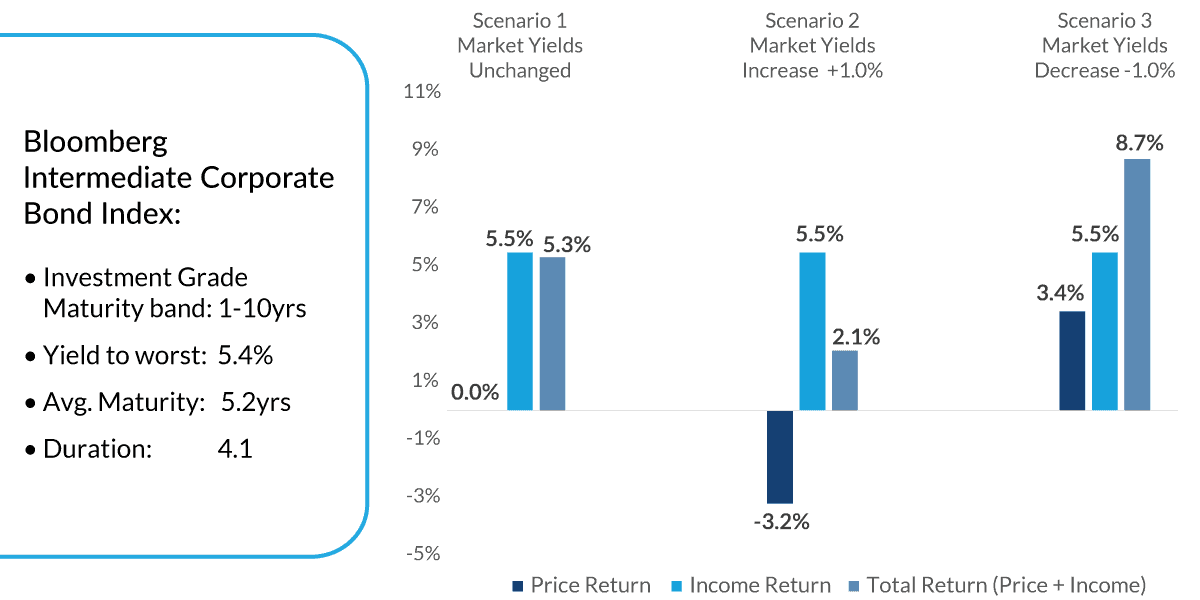

12-Month Risk/Return Analysis

Source: Bloomberg as of 5/31/2024, Bloomberg Intermediate Corporate Index, Investortools Perform.

For illustrative purposes only. Information is subject to change and is not a guarantee of future results.

Chart 5: 2:39– For investors with an extended time horizon, we continue to favor buying longer maturities, as the high levels of income we are seeing are an important source of forward returns that can help cushion the impact of interest rate volatility. To help understand this, we ran the Bloomberg Intermediate Corporate Bond Index through three different interest rate scenarios to estimate forward returns.

If rates remain unchanged over the following 12-month period, bond valuations should remain stable, and total return will likely be driven by yield. Or in other words, the income received is projected to result in a return near 5.3%.

Should rates increase by 1% over the next 12 months, we would expect to see some price depreciation as bond valuations decline, but the income received over this time period should more than compensate for this, and total return would still be positive. Should rates decline by 1%, income and price appreciation would combine for an estimated return near 8.7%.

The key takeaway is if yields move up or down, the distribution of returns remains positive across all scenarios. And the next move from the Fed likely being a rate cut argues for extending maturities. We believe the high levels of income provided by the corporate and municipal bond markets now offer an attractive opportunity for investors. This can help adjust the characteristics of your portfolio in ways that weren’t possible over the past 10 years when yields were much lower.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Actual results, performance or events may differ materially from those expressed or implied in such statements. All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada. City National Bank provides investment management services through its subadvisory relationship with City National Rochdale. Brokerage services are provided through City National Securities, Inc., a wholly-owned subsidiary of City National Bank and Member FINRA/SIPC.

Fixed Income investing strategies & products. There are inherent risks with fixed income investing. These risks include, but are not limited to, interest rate, call, credit, market, inflation, government policy, liquidity or junk bond risks. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed income securities and during periods when prevailing interest rates are low or negative.

Index Definitions:

Bloomberg Intermediate Corporate Bond Index: The Bloomberg Barclays US Intermediate Corporate Bond Index is a measure of the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers that have between 1 and up to, but not including, 10 years to maturity. The maturity range of the bonds included in the index is between 1 to 9.9999 years.

© 2024 City National Rochdale, LLC. All rights reserved.