-

Fixed Income Perspectives

Trade Policy Evolves, Bonds React

May 2025

- Filename

- Fixed Income Perspectives May 2025.pdf

- Format

- application/pdf

TRANSCRIPT

We begin this month’s edition at a time when uncertainty has created historic volatility across the financial markets.

Since early April, wide swings have been driven by tariff-related policies and exacerbated by criticism of Chairman Powell and concerns over the Fed’s independence. Within weeks, however, the tone has cooled, and markets seem to have found some footing. For context, ten-year treasury yields shifted by roughly 50 basis points over the course of a few weeks.

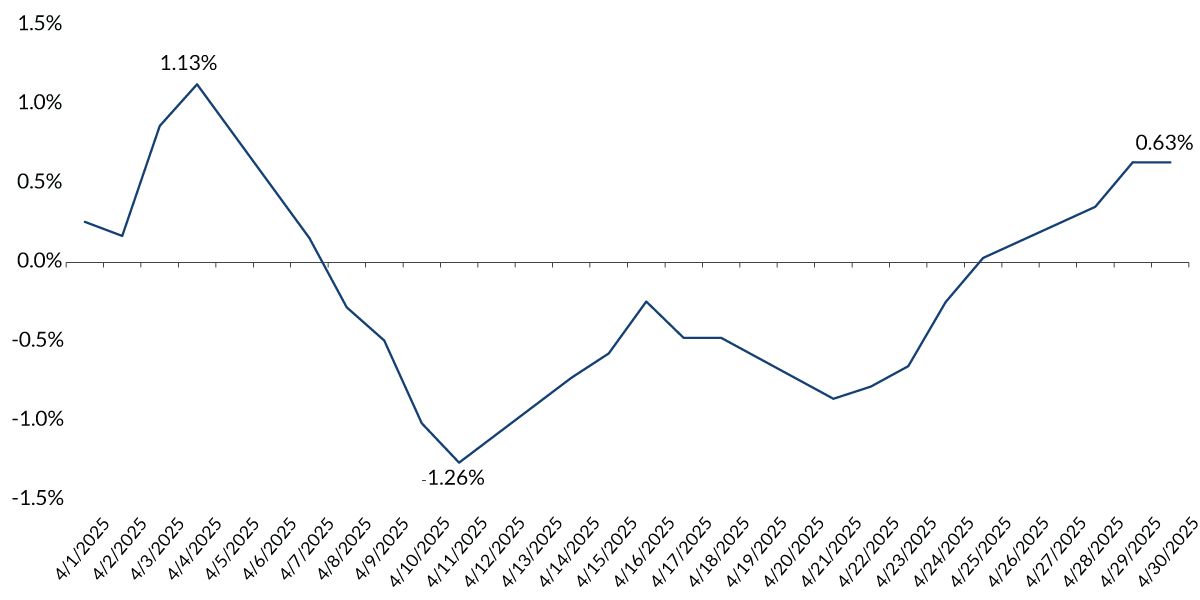

US Treasury Index Total Return

Information is subject to change and is not a guarantee of future results.

Chart 1, 0:42– These sharp yield swings caused the U.S. Treasury index to rise and fall over 1% during the month, before ending in the black. This volatility also had knock-on effects across risk pricing that initially led to a widening of credit spreads that also quickly reversed as sentiment improved. We’ve also observed material changes in technical support across taxable and tax-exempt markets, such as mutual fund flows, which turned negative, but have since stabilized.

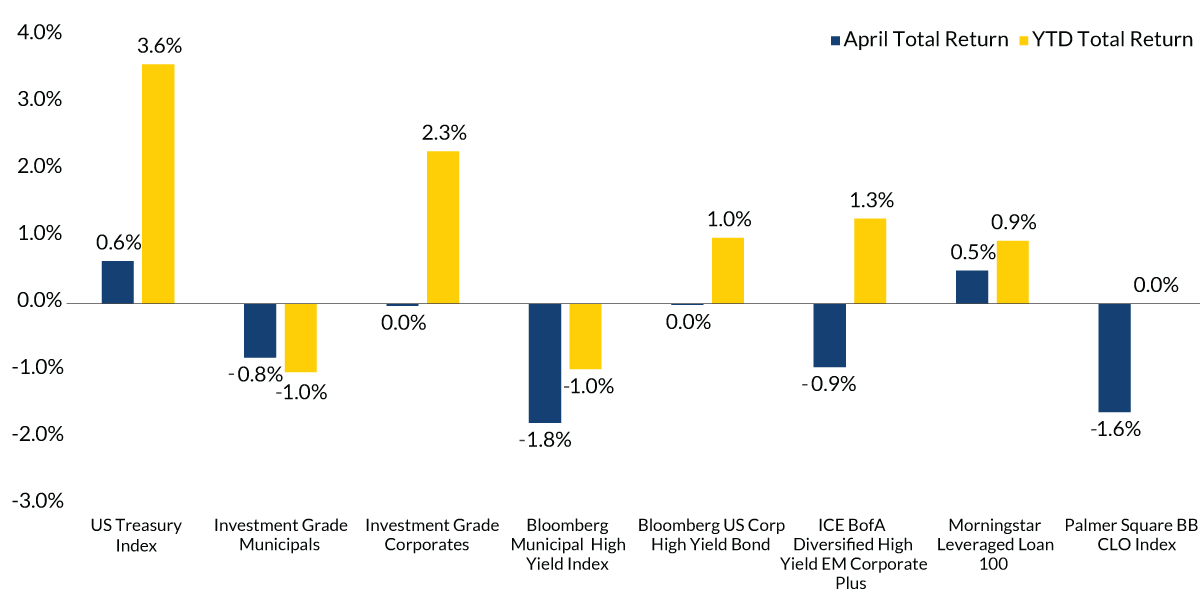

Fixed Income Asset Class Performance

Source: Morningstar Leveraged Loan 100 Index, Bloomberg US Corporate High Yield Index, ICE BofA Diversified High Yield EM Corporate Plus Index, Palmer Square BB CLO Index, Bloomberg Municipal Bond Index, Bloomberg US Treasury Index, Bloomberg High Yield Municipal Bond Index and Bloomberg US Corporate Investment Grade Index as of 4/30/2025.

Information is subject to change and is not a guarantee of future results.

Chart 2, 1:11– Despite these trends, as the dust settled, returns were modestly negative on the month, but remained positive on the year, except for municipal bonds. The April second tariff announcement and ensuing market volatility promoted fears of a sell America narrative, and that foreign buyers were fleeing U.S. debt securities. The ten and thirty-year treasury auctions on April 9 and 10, when yields were surging, intensified the notion that trade policies would erode the attractiveness of U.S. assets.

However, allotment data released after the auctions showed little cause for alarm, as foreign and international interest remained in line with averages since at least January. Further underscoring the support was the strong result of the most recent ten-year auction in early May.

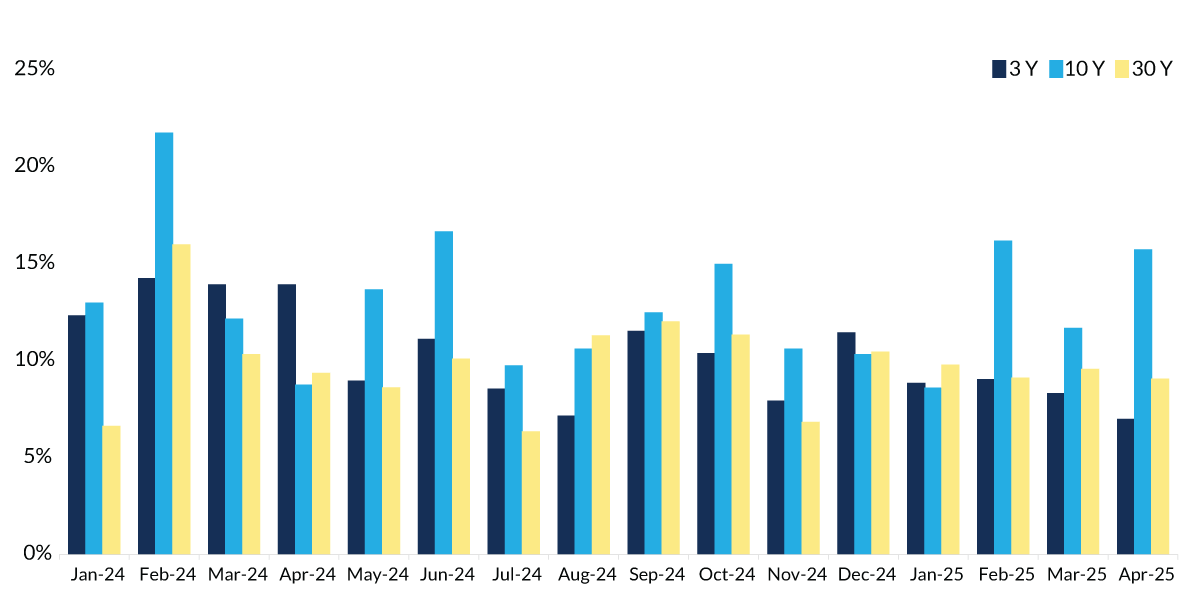

Treasury Auction Allotments to Foreign and International Entities

Source: Bloomberg as of May 12, 2025.

Information is subject to change and is not a guarantee of future results.

Chart 3, 1:55– While longer-term trends have pointed to a reduction in U.S. Treasury holdings over time, recent activity has temporarily alleviated this worry that buyers were avoiding U.S. securities markets. April volatility also spilled over into the municipal market with a roughly 80 basis point rise in yields in just a few days. The significant move in municipals was driven in part by forced ETF and mutual fund selling, a heavy new issue calendar and investor liquidity needs for tax purposes. These events pressured the municipal bond market, but were technical in nature, not the result of a credit stress. The health of municipal bond issuers remains solid, and most sectors are well-positioned to manage through an uncertain federal policy landscape.

Fixed Income Asset Class and Maturity Focus Yield Comparison

Source: Bloomberg 3-month Treasury Bill, Bloomberg Municipal Short/Intermediate Index, Bloomberg Taxable Intermediate Government Credit Index, Bloomberg Municipal High Yield Index, and Bloomberg US Corporate High Yield Index as of 4/30/2025.

Information is subject to change and is not a guarantee of future results.

Chart 4, 2:40– Coupled with attractive higher yields and valuations that remain above recent averages, municipal bonds offer investors in high tax brackets an opportunity to capture compelling tax-efficient cash flow.

As summer approaches, fixed income markets will continue to be shaped by a mix of economic data and evolving trade policies. At the April FOMC meeting, for example, the Fed held rates steady, as expected, but signaled a wait-and-see approach amid uncertainty surrounding tariffs, tax proposals and inflation. Recent economic indicators, particularly the labor market, highlight a stable underlying economy. Trade tensions, including a U.K. deal and constructive dialogue with China, may reduce headline risk and improve market fundamentals. Still, volatility persists across rates. And we maintain our outlook for one-to-two rate cuts this year, with the ten-year yield likely to trade within a 4 to 4.5% range.

Despite this, credit conditions remain solid, especially in investment grade municipal and corporate markets, where we continue to find opportunities we have not seen in at least several years.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

Fixed Income investing strategies & products. There are inherent risks with fixed income investing. These risks include, but are not limited to, interest rate, call, credit, market, inflation, government policy, liquidity or junk bond risks. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed income securities and during periods when prevailing interest rates are low or negative.

Index Definitions:

Bloomberg U.S. Treasury Index: includes all publicly issued, U.S. Treasury securities that are rated investment grade, and have $250 million or more of outstanding face value.

Bloomberg 1-3 Month U.S. Treasury Bill/T-Bill Index (the "Index") is designed to measure the performance of public obligations of the U.S. Treasury that have a remaining maturity of greater than or equal to 1 month and less than 3 months.

Bloomberg U.S. Intermediate Corporate Bond Index measures the performance of U.S. corporate bonds with a maturity of 1–10 years. It's part of the Bloomberg U.S. Corporate Index.

The Bloomberg Municipal Bond: Muni Inter-Short (1-10) Index is a measure of the US municipal tax-exempt investment grade bond market. It includes general obligation and revenue bonds, which both can be pre-refunded years later and get reclassified as such. The effective maturity of the bonds in the index must be greater than or equal to 1 years but less than 10 years.

Bloomberg U.S. Municipal High-Yield Index: covers the U.S.-dollar denominated, non-investment grade, fixed-rate, municipal bond market and includes securities with ratings by Moody’s, Fitch and S&P of Ba1/BB+/BB+ or below.

The Bloomberg US Corporate High Yield Index measures the performance of non-investment grade, US dollar-denominated, fixed-rate, taxable corporate bonds.

ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index tracks the performance of US dollar denominated below investment grade emerging markets non-sovereign debt publicly issued in the major domestic and Eurobond markets.

The Palmer Square CLO Debt Index (“CLO Debt Index”) (ticker: CLODI) is a rules-based observable pricing and total return index for collateralized loan obligation (“CLO”) debt for sale in the United States, original rated A, BBB, or BB or equivalent.

US Corporate Short 1-5 refers to short-term US corporate bonds with 1–5 years remaining until maturity. These bonds are part of the investment-grade corporate bond market, which is dominated by financial services issuers.

Municipal Short 1-5 refers to a collection of municipal bonds that mature between one and five years. These bonds are a type of debt obligation that pay interest that is exempt from federal income tax.

U.S. Corporate Intermediate 1-10 refers to investment-grade corporate bonds that mature between one and ten years. These bonds are denominated in U.S. dollars and are taxable.

Municipal Short/Intermediate 1-10 is a term used to describe a group of US tax-exempt municipal bonds that have a maturity date between one and ten years. These bonds can be used in a variety of investment strategies, including bond ladders and managed accounts.

© 2025 City National Rochdale, LLC. All rights reserved.

Stay Informed.

Get our Insights delivered straight to your inbox.

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.