CNR Speedometers®

December 2023

Forward-Looking Six to Nine Months

TRANSCRIPT

The key takeaway is that, while we have a few changes to review with you, our indicators and recent economic data support our view of a slowing economy in coming months, but do not point to a significant or long-lasting deterioration in economic activity.

■ Previous Month ■ Current Month

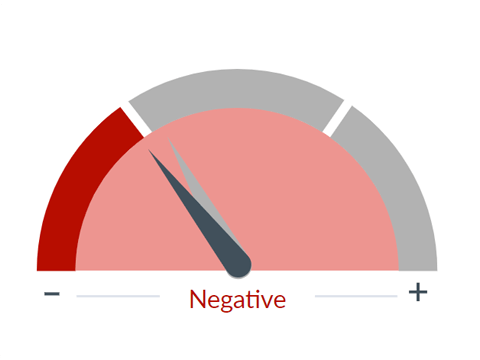

Equity Market Valuation

What we see

Questions of value are always subjective and relative. We believe that equity market valuation should be measured against both the value of stocks at their historical levels and the other investment options available.

Dial 1: Equity Market Valuation 0:33 — Let's start with the two negative changes: firstly, the Equity Valuation dial — we've moved that from the neutral zone back into the negative area.

The recent sharp rally in equity prices has moved the forward Price-to-Earnings (P/E) multiple of the S&P 500 back into the overvalued range at 19 times, well above its historic range of 15.5. Historically, when valuation levels are as high as they are currently, the S&P 500 has experienced a median drawdown of about 14% over the next 12 months, as compared to 5% when valuations are lower.

■ Previous Month ■ Current Month

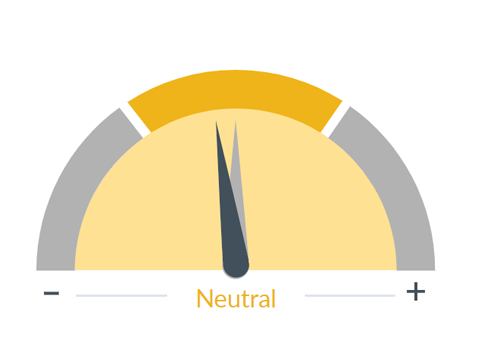

Fiscal Policy

What we see

Changes in tax rates, regulation, and government spending affect the decision-making process of consumers and businesses. By changing tax laws, the government can effectively modify the amount of disposable income available to taxpayers or raise the costs for businesses.

Dial 2: Fiscal Policy 1:08 — The second change we're making is we're keeping the Fiscal Policy dial in the neutral zone but moving the arrow a bit to the left.

In 2023, increased government spending, while adding to the deficit, was a positive contributor to growth of the economy. Going forward, the positive impact from Fiscal Policy is expected to slow.

Looking forward to January and February, it's going to be an important period of time as Congress needs to come to an agreement for the budget for the next fiscal year. If they don't, it will lead to automatic spending cuts that'll take effect in May, resulting in a step down in spending of approximately 0.4% of gross domestic product.

■ Previous Month ■ Current Month

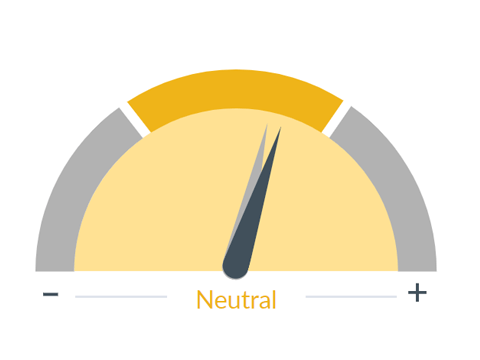

Inflation

What we see

While a slow, persistent rise in prices is consistent with a healthy, growing economy, a rapid increase in inflation, especially if unanticipated, can be harmful. Inflation means higher consumer prices, which often slows sales and reduces profits.

Dial 3: Inflation 1:50 — Now let's shift to three positive changes. We have been shifting the Inflation dial more positively in recent months and are doing so again today. Recent inflation reports continue to move favorably.

The deceleration in the core personal consumption expenditures measure, the key indicator that the Fed looks at, down to 3.5% year over year and 2.4% on a three-month annualized basis, supports our downward glide path expectation.

Now, we have not shifted the dial further to the right, as the battle against deflation isn't over as we see it.

The big concern for Fed officials remains core services ex-housing, the so-called Super Core inflation, and that's tracking at 4.3%, and has been stubbornly high since early 2021 in the 4-5% range, so we're not seeing much progress there.

■ Previous Month ■ Current Month

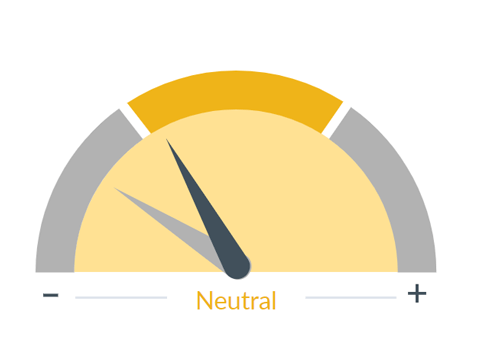

Interest Rates

What we see

Interest rates control the flow of money in the economy. High interest rates curb inflation, but also slow down the economy. Low interest rates stimulate the economy, but could lead to inflation.

Dial 4: Interest Rates 2:44 — Shifting to the Interest Rates dial, we've moved from negative to neutral. While we remain in the “higher for longer” camp as it relates to the Fed funds rate, we continue to believe that barring an unexpected acceleration of inflation, the Fed is done hiking.

Looking forward, we anticipate two rate cuts, but not until the second half of 2024.

Additionally, with the slowing in economic activity (combined with less Treasury issuance), we are expecting that we've likely seen the cycle peak as it relates to the 10-year Treasury yield. As a result of these factors, we've shifted the Interest Rate dial from negative to neutral.

■ Previous Month ■ Current Month

Energy Costs

What we see

Significant changes in energy/oil prices can have important but differing impacts on the overall economy. Higher energy prices act as a tax on consumers and businesses, absorbing money that would normally be used to buy other goods.

Dial 5: Energy Costs 3:24 — On the Energy dial, we are shifting more positively. Despite the ongoing war in the Middle East, crude oil prices have fallen sharply from around $90 a barrel in late September to a new low of around $70.

This slump in energy prices should help lower headline consumer price index inflation, and that's a good thing for the economy.

Summary 3:45 — In conclusion, our Speedometers® and recent economic data support our view of a slowing economy in coming months, but do not point to a significant or long-lasting deterioration in economic activity.