Rochdale Speedometers: May 2026

The key takeaway is: recent data supports our view of a resilient consumer, an economy that’s on solid footing with declining risks of recession, and prospects for two to three cuts by the Fed, so we are once again positively shifting our Speedometers®.

■ Previous Month ■ Current Month

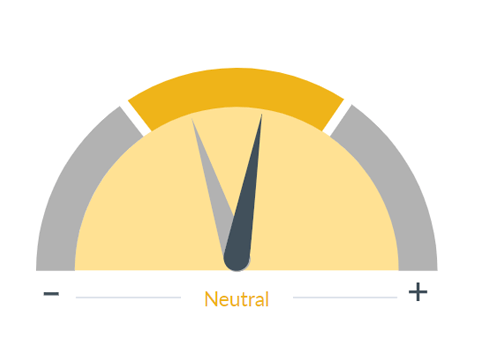

US Economic Outlook

What we see

Timely economic forecasting is very difficult to do but extremely important, especially as the significance of economic information to financial markets continues to rise.

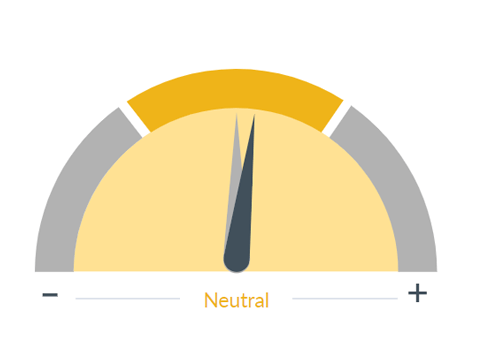

Dial 1: U.S. Economic Outlook 0:32 — Let’s start with the U.S. Economic Outlook dial. The second half of 2023 was stronger than expected, and we entered 2024 on solid footing. While spending by corporations, consumers, and governments are likely to slow in the near term, we are expecting the economy to continue to grow and set the stage for a pickup in the second half of the year, so we’ve shifted our U.S. Economic Outlook dial to the right.

■ Previous Month ■ Current Month

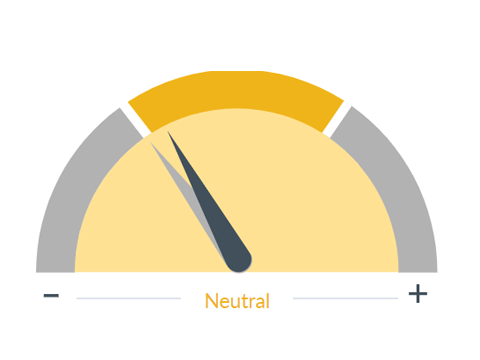

International Economic Outlook

What we see

The world has become increasingly interconnected through trade and the flow of capital, and emerging markets in particular have risen in importance as drivers of global growth. Moreover, we believe a global perspective is integral to any investment strategy.

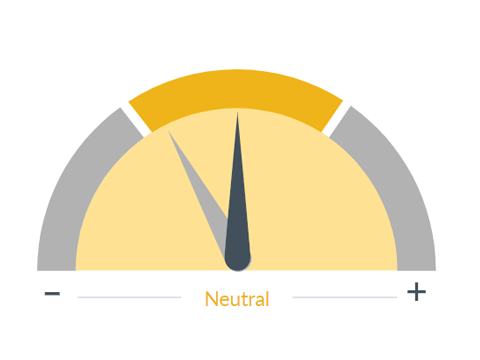

Dial 2: International Economic Outlook 1:01 — Now, because of the strength that we’re seeing in the U.S. economy, we believe, along with others, such as the IMF and the JP Morgan Global PMI composite index, that the outlook for the global economy has improved. So, despite Europe remaining stuck in a “no growth” mode, we’re shifting the Global Economic dial modestly positive.

Shifting to the consumer, as we’ve been discussing, the resilient consumer remains foundational to the strength of the U.S. economy. As a result, we’ve improved several of our consumer-related dials.

■ Previous Month ■ Current Month

Consumer Spending

What we see

Aggregate level of consumer spending. Since consumers are the largest driver of the U.S. economy, their spending patterns have a large impact on overall economic activity.

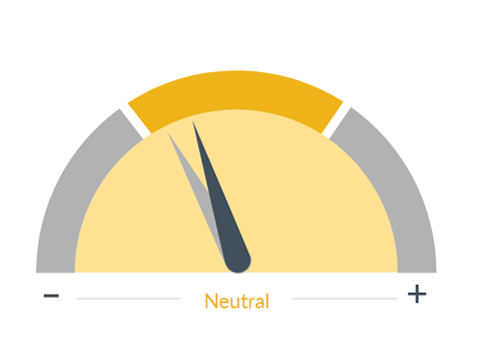

Dial 3: Consumer Spending 1:38 — Consumer spending, while it’s likely to cool in the near term from the target pace we saw in the second half of last year, should remain healthy for the full year as labor markets are strong, wage gains are above inflation, and the positive benefits of the wealth effect remain intact.

■ Previous Month ■ Current Month

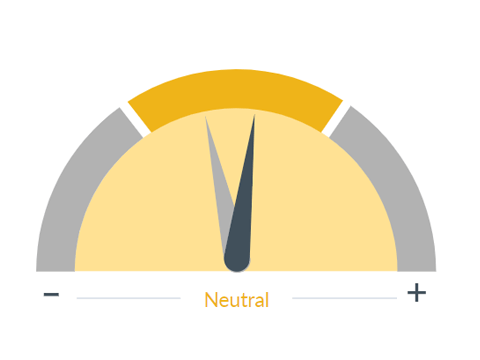

Housing / Mortgages

What we see

Housing is an important indicator of the overall economy and a key driver of investment and job growth. We look at such things as starts, permits, foreclosures, delinquencies, and bank lending to assess the sector's health.

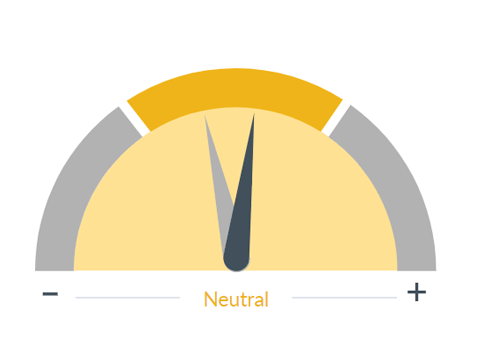

Dial 4: Housing / Mortgages 1:56 — Foundational to the wealth effect is the housing market. We’ve shifted that dial to the right as upward pressure on mortgage rates through the year is expected to moderate, and the supply demand balance should keep housing prices on an upward path.

■ Previous Month ■ Current Month

Consumer Sentiment

What we see

How consumers feel about their overall financial health as well as that of the economy on the short and long term. This is an important indicator, as the consumer is the largest driver of the U.S. economy.

Dial 5: Consumer Sentiment 2:12 — For two months in a row, we have seen improved measures of consumer sentiment – the largest change in over 30 years, and this trend is likely to continue positively through the year from the wealth effect, solid income dynamics, as well as the downward glide path of inflation and those Fed cuts.

■ Previous Month ■ Current Month

Credit Demand / Availability

What we see

Availability of credit from banks and the overall financial sector to provide capital to the economy. Restrictive credit conditions are a headwind to economic activity, while accommodating conditions may boost it.

Dial 6: Credit Demand / Availability 2:30 — On the corporate side, while the banking industry continues to be challenged by a multitude of issues in the short term, it is encouraging that the pace of banks that are tightening their lending standards has slowed. And with the prospects for two to three rate cuts in the second half of the year, a modest pickup in the economy in the second half should lead to firmer demand for loans, which the lending officer survey also confirmed. This, combined with solid availability from private credit sources, is why we’ve shifted that dial to the right.

■ Previous Month ■ Current Month

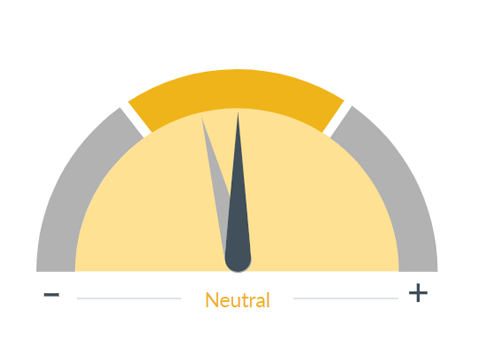

Business Outlook Spending/Surveys

What we see

Surveys of the business community on current and expected trends. This is a gauge on businesses' spending plans that provides an insight into wages, inflation, and capital equipment spending.

Dial 7: Business Outlook Spending / Surveys 3:05 — While in the near term, certain industries are pairing back plans for capital spending, others are increasing, and there are nascent signs that the moribund manufacturing sector could start to come to life in coming months. So, the appetite for business investment should also be improving in the next six to nine months.

■ Previous Month ■ Current Month

Corporate Profit Growth

What we see

Corporate earnings have a significant influence on the stock market as they ultimately drive stock prices. The value of securities is the present value of all future cash flows.

Dial 8: Corporate Profit Growth 3:23 — Lastly, while expectations for consensus EPS growth have moderated for 2024, with a better outlook for the economy, there is increasing visibility in the outlook for earnings growth, so we’re tweaking the Corporate Profitability dial.

So, in conclusion, we are once again positively shifting our Speedometers® to reflect the benefits of a resilient consumer, an economy on solid footing with declining risks of recession, and prospects for two to three rate cuts by the Fed in the second half of this year.