Rochdale Speedometers: May 2026

From all of us at CNR, we wish everyone all the best for a healthy and prosperous new year.

The key takeaway for this month is that, while economic activity is expected to slow in the near term, barring any unexpected significant exogenous geopolitical shocks — and lord knows there's many of them to be worried about these days — the downside risk to the economy continues to diminish, and the outlook over the next six to nine months continues to improve.

■ Previous Month ■ Current Month

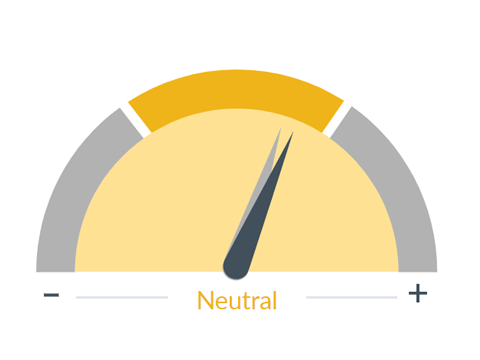

Inflation

What we see

While a slow, persistent rise in prices is consistent with a healthy, growing economy, a rapid increase in inflation, especially if unanticipated, can be harmful.

Dial 1: Inflation 0:48 — Let's start with the Inflation dial, the most important one. Continuing the trend of the last few months, we are once again shifting the inflation dial to the right, as recent reports indicate the downward glide path of inflation has been better than expected.

Most importantly, the Fed's preferred measure of inflation, the Core PCE, showed modest month-to-month growth at only 0.1%, and now stands at 3.2% year over year. We're expecting this downward trend to continue.

This should enable the Fed to cut interest rates in the second half of 2024, and we're now anticipating two to three cuts by the end of the year.

■ Previous Month ■ Current Month

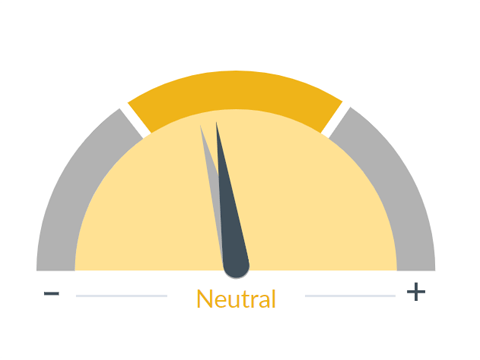

Housing / Mortgages

What we see

Housing is an important indicator of the overall economy and a key driver of investment and job growth. We look at such things as starts, permits, foreclosures, delinquencies, and bank lending to assess the sector's health.

Dial 2: Housing / Mortgages 1:30 — Shifting to the Housing Market dial, we’re shifting that one modestly to the right as well. While the current challenges of affordability, tight inventory and high prices remain, with inflation trending lower over the next six to nine months, lower mortgage rates are likely to follow them down. This should provide a modestly positive impact to the economy in the next six to nine months.

■ Previous Month ■ Current Month

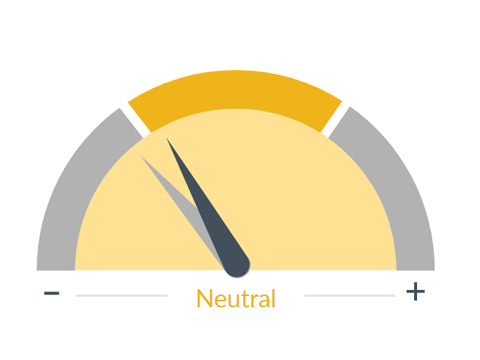

Credit Demand / Availability

What we see

Availability of credit from banks and the overall financial sector to provide capital to the economy. Restrictive credit conditions are a headwind to economic activity, while accommodating conditions may boost it.

Dial 3: Credit Demand / Availability 1:54 — We're also shifting the Credit Demand and Availability dial from red into the yellow zone. While loan demand should continue to slow in the near term, and delinquencies will continue to pick up from historically low levels, we may be coming close to the peak in the tightening of lending standards as deposit runoff has slowed, and net interest margins are starting to stabilize.

Additionally, non-bank lenders have not tightened their lending standards nearly as much as the banks, and they have an abundant amount of capital to deploy, so the flow of the economy of credit into the economy may be different, and we may be bottoming out and likely to improve.

■ Previous Month ■ Current Month

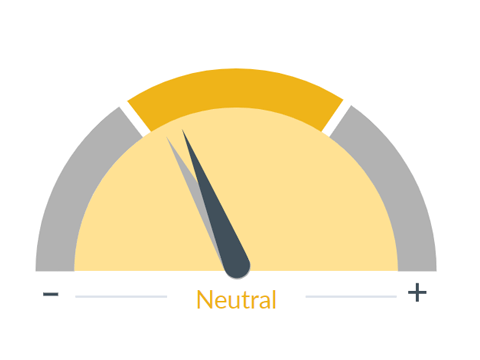

Business Outlook

What we see

Surveys of the business community on current and expected trends. This is a gauge on businesses' spending plans that provides an insight into wages, inflation, and capital equipment spending.

Dial 4: Business Outlook Spending/Surveys 2:35 — Shifting to the Business Outlook dial, we've tweaked that one more positively as well. While the recent surveys of capital spending plans by small businesses remain subdued in the near term, the recent ISM manufacturing report fell for the 14th consecutive month. Now there was good news in that report, in that the majority expect stronger business activity in the second half of 2024.

Add all these dial changes and factors together, the U.S. economic outlook continues to improve, and we've moved that dial as well.

Labor markets remain solid, average hourly earnings, as we've just seen, came in at 4.1%, which is above inflation levels, which should ease pressure on summer’s spending and sentiment.

As a result, the risks of a mileage session in the first part of the year have declined yet again to around 50%.

Once we get through this near-term slowdown, the stage should be set for improvements looking at six to nine months.

■ Previous Month ■ Current Month

Corporate Profit Growth

What we see

Corporate earnings have a significant influence on the stock market as they ultimately drive stock prices. The value of securities is the present value of all future cash flows.

Dial 5: Corporate Profit Growth 3:35 — Lastly, shifting to Corporate Profits, the upcoming earning season is going to be a very important one. Now, because estimates for the fourth quarter declined so much after Q3, the bar has been lowered quite a bit. So we're not overly concerned about the reported results, but with economic growth around the world slowing, guidance from companies for 2024 will likely be on the cautiously optimistic side, and consensus estimates may have to come down closer to our levels.

Now, we are tweaking the corporate profit dial modestly to the right, anticipating that earnings growth will improve in the second half of 2024 along with an improved economic environment.

The key takeaway from this month is, barring any unexpected, significant exogenous shocks, downside risks of the economy continue to diminish, and the outlook over the next six to nine months continues to improve.