Rochdale Speedometers: May 2026

Over the past year, one of the biggest surprises wasn’t really about the economy — it was about leadership. As policy shifted and capital began to move, investors were forced to rethink long-held assumptions about global markets. The U.S. still matters, but global markets delivered a clear reminder: Performance doesn’t come with a passport. As we head into 2026, the conversation will start to move away from “Is the U.S. the only place to invest?” and toward a more practical question: Where is the money flowing — and why? So before jumping straight into dials and decimals, let’s briefly put a bow on 2025 — because the lessons from last year matter greatly for how we’re positioning today.

We believe there are three big themes that defined markets in 2025, whether investors realized it at the time or not.

The first was resilience without momentum. The U.S. economy never broke — but it never really took off, either. Growth stabilized, inflation cooled, employment softened at the margin, but consumption kept going. It wasn’t a boom, it wasn’t a bust — it was a year where the economy simply refused to behave the way either optimists or pessimists expected. That forced markets to reprice extremes on both sides.

The second theme was policy noise versus policy math. 2025 produced no shortage of headlines — tariffs, fiscal packages, Fed commentary, geopolitics — but the actual macro impulse from policy ended up being far more modest than feared. Fiscal policy didn’t collapse growth, tariffs didn’t reignite inflation and monetary policy quietly shifted from restrictive toward neutral. A lot of investors reacted emotionally to the headlines; fewer stuck with the arithmetic.

And the third defining feature of 2025 was markets learning to live with valuation. Equities stayed expensive — but earnings didn’t roll over. Returns came less from multiple expansion and more from profits simply showing up. That’s an important distinction, because it’s one reason markets felt fragile even when they were working.

Those three themes — resilience without momentum, noisy policy with modest impact and expensive but earnings-supported markets — are what we’re carrying forward into January. Now, looking ahead, 2026 is shaping up very differently, and we think there are two big ideas that will matter most for portfolios.

The first is that fiscal and monetary policy risk may begin to flip.In 2025, policy uncertainty functioned as a persistent headwind. Tariffs, executive actions and shifting expectations around the Federal Reserve created ongoing friction — even as the economy proved more resilient than many feared. Looking ahead to 2026, that backdrop has the potential to evolve. Uncertainty around tariffs appears to be diminishing, the drag from policy ambiguity may begin to fade and the focus is likely to shift toward deregulation and policy implementation rather than headline risk. At the same time, monetary policy is moving away from a restrictive stance, meaning the direction and pace of Fed decisions may matter more than the absolute level of interest rates. Policy risk does not disappear — and in fact, easing too quickly becomes a meaningful concern — but its character changes. What has been a constant obstacle may instead become a conditional tailwind that is dependent on execution over rhetoric.

The second big idea is that growth becomes more self-sustaining — and more global. Entering 2026, the drivers of growth matter less because of U.S. stimulus and more because capital is being deployed where fiscal support is expanding. Corporate investment, productivity and balance-sheet strength remain important, but the incremental impulse increasingly comes from outside the U.S. Many international markets are entering a phase of fiscal spending — on defense, infrastructure, energy and industrial policy — that simply isn’t likely to materialize in the same way in the U.S. Following the money has historically driven relative performance, and that dynamic becomes more relevant as the U.S. steps back from its role as the world’s de facto global insurer. As that responsibility diffuses, other regions are forced to spend, invest and stimulate domestically — creating a more diversified and, in some cases, more powerful growth impulse. This doesn’t mark the end of U.S. leadership, but it does mark a shift toward a more balanced global growth backdrop, where opportunities are increasingly shaped by where fiscal capacity is being deployed rather than where capital has been concentrated historically.

Now, a quick note on positioning: After a strong run in technology, we think it’s wise to be thoughtful about how returns are generated from here. Technology remains a critical driver of earnings and innovation, but the current setup looks familiar — leadership is narrow, valuations are elevated and risk is increasingly concentrated. In environments like this, maintaining returns often means complementing U.S. exposure with international markets that are less technology-heavy, more defensive in composition, and historically inexpensive relative to the U.S. This isn’t about abandoning what’s worked, but about recognizing that a similar market setup has, in the past, rewarded broader and more diversified sources of return.

Turning to the dials — and keeping it practical — we made two changes in January: housing and corporate profits.

■ Previous Month ■ Current Month

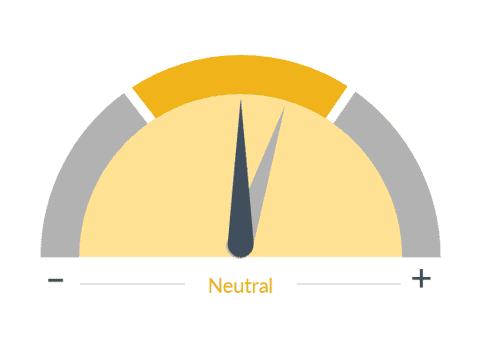

Housing / Mortgages

What we see

Housing is an important indicator of the overall economy and a key driver of investment and job growth. We look at such things as starts, permits, foreclosures, delinquencies, and bank lending to assess the sector's health.

Dial 1: Housing / Mortgages, 5:51— Starting with a downgrade for housing. It has quietly shifted from being a stabilizer to being more of a constraint. This isn’t about supply — it remains structurally tight. The issue is affordability. We believe rates will be stubborn in 2026 and the reset in home prices hasn’t fully caught up with income reality. Activity has slowed, turnover remains muted and housing is no longer providing the same cushion to growth that it did earlier in the cycle. That’s why we moved the housing Speedometer to neutral this month — not because we see a collapse, but because its contribution to the equity environment has faded.

■ Previous Month ■ Current Month

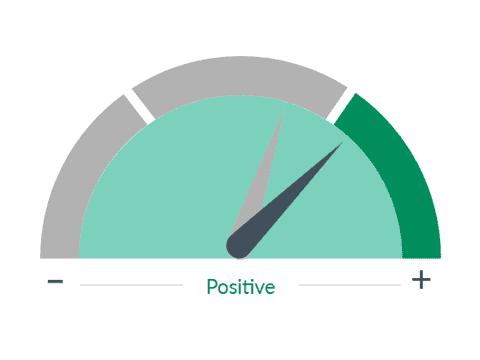

Corporate Profit Growth

What we see

Corporate earnings have a significant influence on the stock market as they ultimately drive stock prices. The value of securities is the present value of all future cash flows.

Dial 2: Corporate Profit Growth, 6:31— On the other hand, corporate profits have earned an upgrade for the second month in a row. Margins have held up better than expected, pricing power hasn’t disappeared, and earnings breadth has quietly improved. This isn’t just a mega-cap story anymore. Capital discipline, productivity gains and technology-driven efficiency are showing up in results. That’s an important offset to high valuations, and it’s why the corporate profits dial moved higher and turned green this month.

Stepping back, that combination — softer housing, stronger profits — tells you something important about where we are in the cycle. Growth is rotating, not collapsing. The economy is adjusting, not breaking. And equity risk is increasingly about expectations, not fundamentals —a key to our belief that investors should be more diversified.

So, what does this mean for your portfolio?

It means we still respect valuation. It means we still expect volatility around policy and geopolitics. But it also means we’re increasingly focused on durability over drama — earnings power, balance sheets, and areas of the market where growth doesn’t require heroic assumptions. So as we officially send off 2025 — a year of resilience, noise and adjustment — we head into 2026 with a clearer roadmap. Not euphoric. Not fearful. Just disciplined, selective and increasingly focused on where improvement is most likely to show up.

RBC Rochdale, LLC. is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

Rochdale Speedometers are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect RBC Rochdale’s overall outlook of the economy.

RBC Rochdale, LLC., its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

©2026 RBC Rochdale, LLC. All rights reserved.