CNR Speedometers®

June 2025

Forward-Looking Six to Nine Months

TRANSCRIPT

Our investment committee conversation was spirited this month as the market environment continues to change, but we did not make any dial changes this month. There's no shortage of headlines to work through, from inflation trends and equity valuations to the latest twists in fiscal policy and trade. While the noise level is still high, the reality beneath the surface may not be as concerning as it's been made out to be.

■ Previous Month ■ Current Month

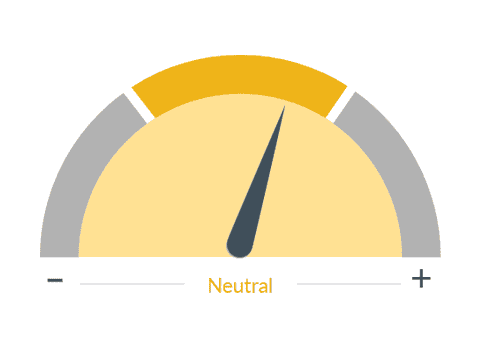

Inflation

What we see

While a slow, persistent rise in prices is consistent with a healthy, growing economy, a rapid increase in inflation, especially if unanticipated, can be harmful. Inflation means higher consumer prices, which often slows sales and reduces profits. Higher prices often lead to higher interest rates. Over time, inflation can also wear away at the value of stocks, which is why it is crucial to monitor.

Dial 1: Inflation, 0:34— So, let's start with inflation. The latest CPI and PPI data came in softer than expected, with both showing declines month over month. Now, that's encouraging, but we're not ready to call it a turning point just yet.

Expectations around inflation have really gotten out of hand. Survey data has priced in an extreme scenario driven by tariffs, but we think that's overstated. In fact, the inflationary impact of tariffs is often misunderstood.

Imports make up roughly 10% of the inflation calculation, so even a 1% increase in the effective tariff rate would only push up inflation higher by about 0.1%. Now that's not insignificant, but it's far from a runaway inflation story. We're also watching the legal backdrop. Core challenges to the administration's use of emergency powers for tariffs could limit its ability to impose new ones or retaliate further. Add to that some clear signs that according to the administration, China may not be honoring the terms of the recent trade truce, and it's a murky picture. But again, the takeaway here is that inflation risk may not be as severe as the current market tone suggests.

The Fed, meanwhile, is standing by. The latest FOMC minutes emphasized that the committee is well positioned to wait for more clarity.

Policymakers still see a risk that inflation proves sticky, but they're not rushing to act. We continue to expect one to two rate cuts later this year, though the Fed is watching the data closely and will need more confirmation before moving.

■ Previous Month ■ Current Month

Equity Market Valuation

What we see

Questions of value are always subjective and relative. We believe that equity market valuation should be measured against both the value of stocks at their historical levels and the other investment options available. A stock is worth its future earnings, but that involves a degree of uncertainty, which affects its price depending on the degree.

Dial 2: Equity Market Valuation, 1:59— On the equity front, valuations have come down a bit — not to levels we'd call “attractive” across the board, but directionally better. Markets have stabilized following a sharp run-up earlier in the year. And sector performance has become more dispersed, which is a healthy sign and opens the door for more selective opportunities.

Tech is still expensive, but other sectors continue to reflect better relative value. Corporate earnings in Q1 were a clear highlight, growing at about 13% and doubling pre-season expectations. While companies are still cautious in their outlooks, they're generally managing well through policy and cost volatility so far.

The market seems to be adjusting, too. It's no longer reacting as sharply to negative headlines, while still responding positively to good news. That shift in tone reflects how much uncertainty has already been priced in.

Shifting to global equity returns year to date, one of the most striking dynamics is the role of currency.

Much of the performance, especially outside of the U.S., has been driven less by earnings or economic growth and more by exchange rate movements. In Europe and other developed markets, returns have been amplified by the weakening U.S. dollar, which boosts the value of foreign assets in dollar terms. That currency tailwind can create the illusion of stronger fundamentals, but underneath, the picture is more mixed. In fact, when you strip out currency effects, the actual local returns in many international markets are far more modest.

This highlights why we haven't made an international move yet, and it's also a reminder that in this environment, the dollar itself is a key driver of portfolio performance. In fact, it may be the most important factor in equity returns for the rest of this year. So all in all, we think this is a good time to take stock of broad asset allocation.

Equity markets have run up fast. And while we're not bearish, we are leaning more conservative when it comes to adding risk.

■ Previous Month ■ Current Month

Fiscal Policy

What we see

Changes in tax rates, regulation, and government spending affect the decision-making process of consumers and businesses. By changing tax laws, the government can effectively modify the amount of disposable income available to taxpayers or raise the costs for businesses. However, this process takes time, as the money needs to wind its way through the economy, creating a significant lag between the implementation of fiscal policy and its effect on the economy.

Dial 3: Fiscal Policy, 3:47— One area we seriously debated downgrading was fiscal policy.

So far, the administration's efforts have been underwhelming. Expectations for a sweeping pro-growth agenda haven't materialized.

The policies that have been rolled out, including the new tax bill, haven't lived up to the early hopes for meaningful business stimulus. Now, that said, we are monitoring potential executive actions that could improve the picture, especially in the financial sector.

One area to watch is the supplementary leverage ratio (SLR). This is a rule that requires banks to keep a certain amount of capital on hand, no matter how risky or safe their assets are. It was put in place after the 2008 financial crisis to help limit bank risk taking. And there's speculation that the administration may reduce the SLR to free up capital and support lending, especially when it comes to U.S. Treasury issues.

If that happens, it could provide some lift to financials and credit conditions more broadly. But for now, it's just talk. And the broader theme remains: We've seen less action and more noise than investors had hoped when it comes to the business climate.

So where do we stand overall? Inflation isn't fixed, but it's not spiraling. Valuations aren't cheap, but they're more reasonable. Fiscal policy has been a letdown so far, but there still may be catalysts ahead. And most importantly, the market has digested a lot of headline risk, which means we may be through the worst of the volatility phase — at least for now.

So, we continue to see U.S. growth holding above 1%, with solid support from the labor market and strong Q1 earnings. But with higher interest rates, geopolitical friction, and policy uncertainty still in the mix, we remain focused on protecting capital and being selective in how we take risks.

Important Information

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

CNR Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect City National Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

City National Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and City National Rochdale are subsidiaries of Royal Bank of Canada.

©2025 City National Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE