-

Fixed Income Perspectives

The Treat, Not the Trick

October 2025

- Filename

- Fixed Income Perspectives OCTOBER 2025.pdf

- Format

- application/pdf

TRANSCRIPT

In what is shaping up to be a strong year for fixed income, the third quarter delivered another period of broad-based positive returns across all major sectors. Performance was supported by resilient corporate earnings, easing trade tensions, as well as prospects for a rebound in economic growth.

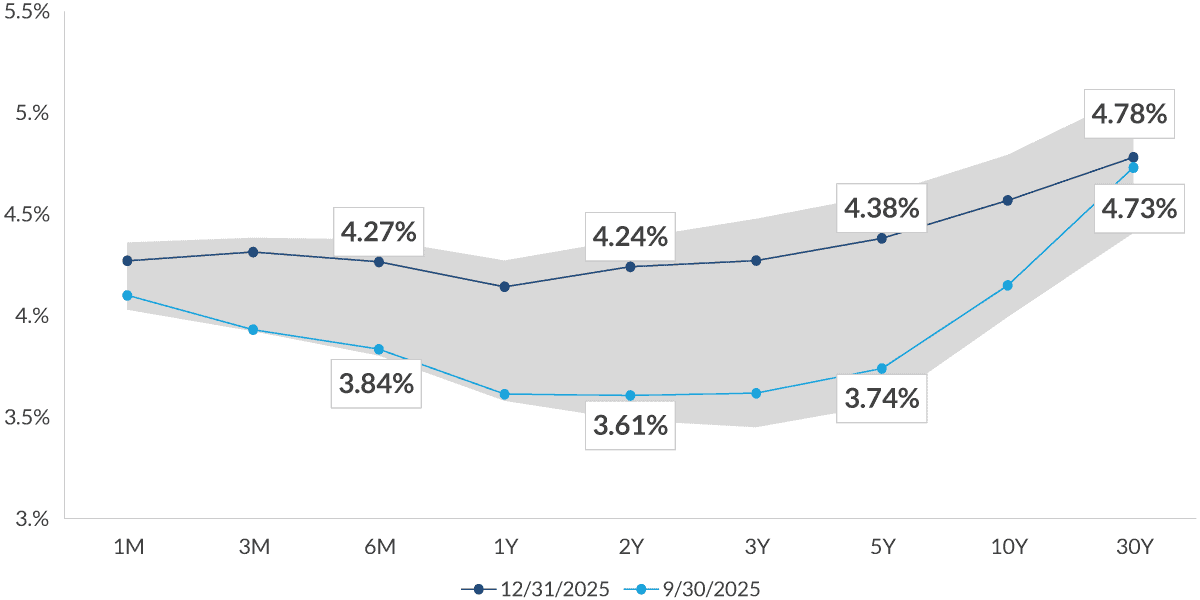

Yield Curve

Source: Bloomberg US Treasury Curve as of 9/30/2025. Grey area represents the range of yields in the respective portion of the curve.

Information is subject to change and is not a guarantee of future results.

Chart 1, 0:32– By quarter-end, signs of labor market cooling and subdued inflation allowed the Federal Reserve to reduce the policy rate by 25 basis points. As a result, U.S. Treasury yields declined modestly across the curve. With year-to-date levels remaining lower overall—most notably in the shorter, policy-sensitive maturities.

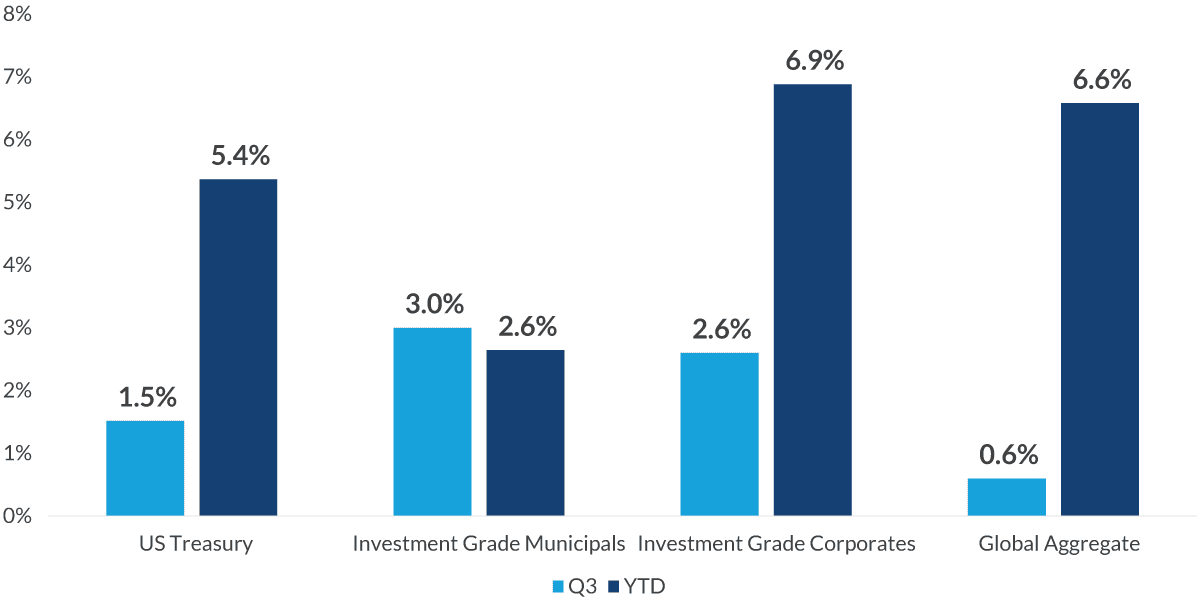

Investment Grade Total Returns

Sources: Bloomberg US Treasury Total Return Unhedged Index, Bloomberg Municipal Bond Index, Bloomberg US Corporate Total Return USD Index, Bloomberg Global Aggregate Total Return Value Unhedged Index as of 9/30/2025.

Past performance is not a guarantee of future results.

Chart 2, 0:54– Within the investment-grade markets, municipal bonds sprung back to life with a 3% return in the quarter—outpacing most sectors, including U.S. Treasuries and corporates.

This outperformance was primarily driven by steady demand for longer-duration paper, as valuations and tax-adjusted yields became very attractive for investors seeking tax-efficient income. Like municipals, credit spreads, or the extra yield earned for risk, tightened in the corporate bond space, helping this market gain further ground with YTD returns close to 7%. While global markets returned just 60 bps in the quarter, performance to date remains healthy and continues to benefit from early-year weakness in the dollar.

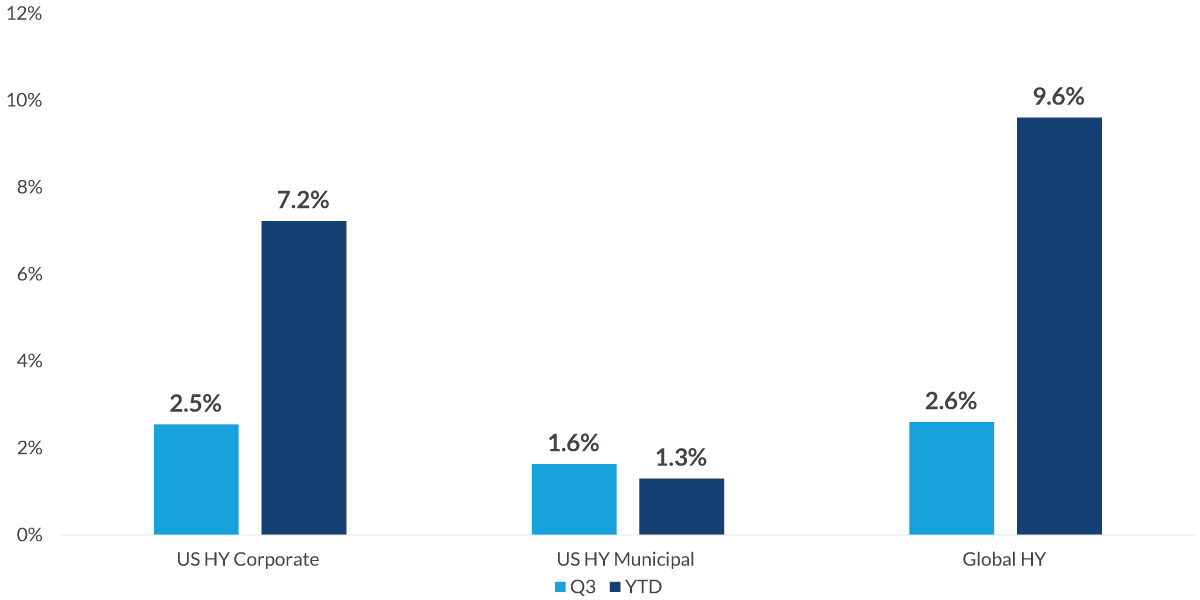

High Yield Total Returns

Sources: Bloomberg US High Yield Total Return Unhedged USD Index, Bloomberg High Yield Municipal Bond Index Total Return Index Value Unhedged USD, Bloomberg Global Aggregate High Yield Total Return Value Unhedged USD Index as of 9/30/2025.

Past performance is not a guarantee of future results.

Chart 3, 1:36– Turning our attention to global and U.S. high yield, these markets returned approximately 2.5% in the third quarter. On a year-to-date basis, global high yield continues to outperform, helped by attractive starting yields, durable credit fundamentals, as well as early-year dollar weakness. Institutional flows have also been positive, reflecting confidence in this market.

A bright spot during the quarter was U.S. high-yield municipal bonds, which turned positive for the year in September with performance of about 2.6%. This was the highest monthly return for the period since 2013. With taxable equivalent yields above 9.5%, high-yield municipals remain a highly competitive alternative to taxable options.

As we enter the final months of the year, the shutdown has been top of mind for investors, but it has not materially affected the financial markets to date. In the near term, we anticipate little impact on bonds with the debt ceiling having already been addressed. History has shown that government shutdowns may generate volatility in the short run, especially as jobs and inflation data are delayed, but any decline in the markets tends to recover quickly.

From our perspective, we continue to watch the data and believe underlying trends point to a cooling but stable economy—allowing the Fed to cut rates 1-2 more times this year—and continue toward policy normalization into 2026.

Over the past 18 months, we have maintained our 10-year forecast at 4-4.5%. We now see a path for longer-term rates to gradually move lower, and we have revised our range down to 3.75-4.25%.

Finally, we remain broadly positive on fixed income and see the potential to add to what has already been a strong year across the various markets. While we continue to remain cautious on corporates where credit spreads remain tight, we expect carry will be the dominant driver of return over the near term. Additionally, municipals continue to offer a compelling opportunity with strong credit fundamentals, heavy supply and attractive tax-adjusted yields.

Important Information

The views expressed represent the opinions of RBC Rochdale, LLC which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Rochdale believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

RBC Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

Fixed Income investing strategies & products. There are inherent risks with fixed income investing. These risks include, but are not limited to, interest rate, call, credit, market, inflation, government policy, liquidity or junk bond risks. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed income securities and during periods when prevailing interest rates are low or negative.

High yield securities. Investments in below-investment-grade debt securities, which are usually called “high yield” or “junk bonds,” are typically in weaker financial health. Such securities can be harder to value and sell, and their prices can be more volatile than more highly rated securities. While these securities generally have higher rates of interest, they also involve greater risk of default than do securities of a higher-quality rating.

Index Definitions:

The Bloomberg US Treasury Curve refers to a graphical representation of interest rates on U.S. Treasury debt across various maturities, showing the yield an investor receives for holding short-term versus long-term government bonds at a specific point in time.

The Bloomberg US Treasury Total Return Unhedged Index measures the total return of US dollar-denominated, fixed-rate, nominal US Treasury securities with at least one year of remaining maturity, excluding bills and inflation-linked bonds, without applying currency hedging to US dollar-based investors. The "total return" reflects both interest payments and price changes, while "unhedged" signifies that currency fluctuations are not accounted for.

The Bloomberg Municipal Bond: Muni Inter-Short (1-10) Index is a measure of the US municipal tax-exempt investment grade bond market. It includes general obligation and revenue bonds, which both can be pre-refunded years later and get reclassified as such. The effective maturity of the bonds in the index must be greater than or equal to 1 years but less than 10 years.

The Bloomberg US Corporate Total Return USD Index measures the performance of the investment-grade, fixed-rate, taxable corporate bond market, including securities denominated in U.S. dollars (USD) and publicly issued by U.S. and non-U.S. industrial, utility, and financial companies.

The Bloomberg Global Aggregate Total Return Value Unhedged Index is a multi-currency, investment-grade fixed-rate bond index that includes government, government-related, corporate, securitized (mortgage-backed, asset-backed, and commercial mortgage-backed) bonds from both developed and emerging markets, with the "unhedged" aspect meaning it does not account for foreign currency fluctuations, providing a measure of global debt performance without the impact of currency hedging.

The Bloomberg High Yield Municipal Bond Index Total Return Index Value Unhedged USD is a market-value-weighted index that measures the total return performance of the non-investment-grade, long-term, fixed-rate, tax-exempt U.S. municipal bond market, calculated in U.S. dollars without accounting for currency hedging. It includes securities from all U.S. states, Washington D.C., Puerto Rico, Guam, and the Virgin Islands, covering both general obligation and revenue bonds.

The Bloomberg Global Aggregate High Yield Total Return Value Unhedged USD Index tracks the performance of global, fixed-rate, high-yield debt securities, including U.S., European, and Emerging Market issues, denominated in U.S. Dollars without currency hedging, and includes both principal and interest payments in its total return calculation. It represents the high yield market by combining the U.S. Corporate High Yield, Pan-European High Yield, and Emerging Markets Hard Currency High Yield indices.

© 2025 RBC Rochdale, LLC. All rights reserved.

Stay Informed.

Get our Insights delivered straight to your inbox.

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.