-

Fixed Income Perspectives

The Policy Pivot Has Arrived

September 2024

- Filename

- Fixed Income Perspectives SEPTEMBER 2024.pdf

- Format

- application/pdf

TRANSCRIPT

In what has been the most uncertain run up to a Fed meeting in some time, with market participants agreeing a rate cut was in the cards, but divided on the magnitude, the long-awaited start to the Fed easing has begun.

At its September meeting, the Federal Reserve decided to go big, lowering the federal funds rate by 50 basis points to a range of 4.75% – 5%. For the first time since 2005, the decision was not unanimous, with one committee member dissenting in favor of a 25-basis point cut. Overall, the 50-basis point move signals that the Fed remains concerned about the labor market risks but acknowledges inflation is moving toward its policy goal and that the economy remains on solid footing.

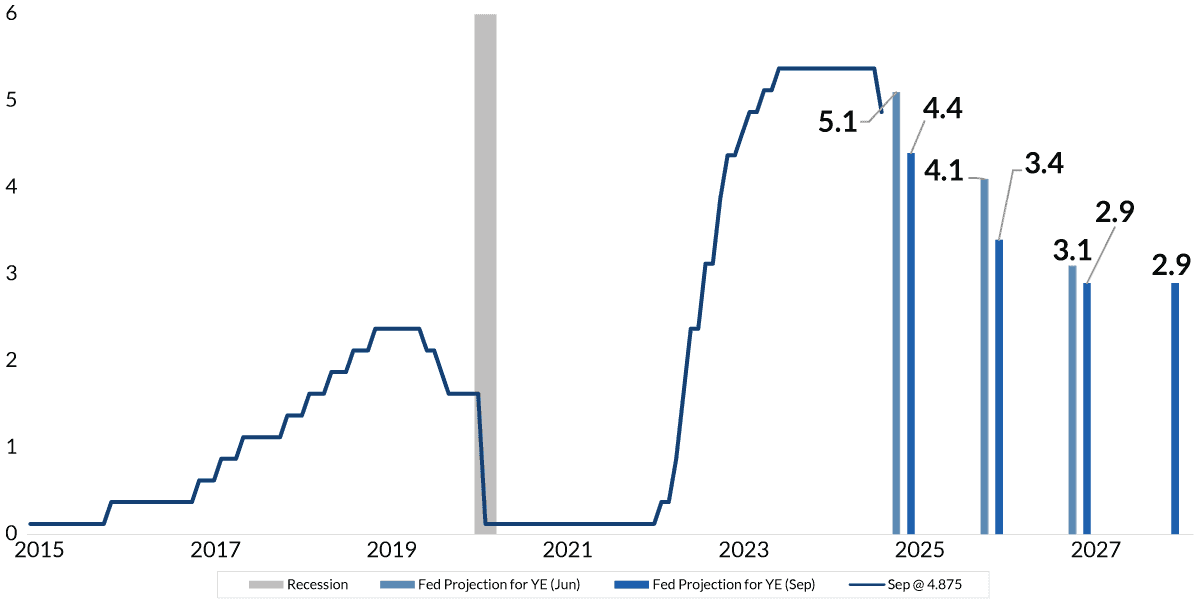

FOMC Projections - Federal Funds

%, mid-point

Sources: Bureau of Economic Analysis; FOMC as of September 18, 2024.

Information is subject to change and is not a guarantee of future results

Chart 1, 0:58– Policymakers also updated expectations for the federal funds rate over the next several years. Federal Reserve members now expect an additional 50 basis points of easing by year end and another 100 basis points in 2025. Expectations for the longer-term fed funds rate are now slightly higher at 2.9%, up 10 basis points from the previous meeting. This suggests revised rates should continue to support growth.

More balanced risks between inflation and employment were evident in the economic projections. The median projection for unemployment at the end of 2024 rose to 4.4% from 4% in the June forecast, a small deterioration from current levels. The median forecast for inflation at year end declined to 2.3% with inflation not returning to the Fed’s 2% target until at least 2026. Economic growth projections also moved down slightly to 2%.

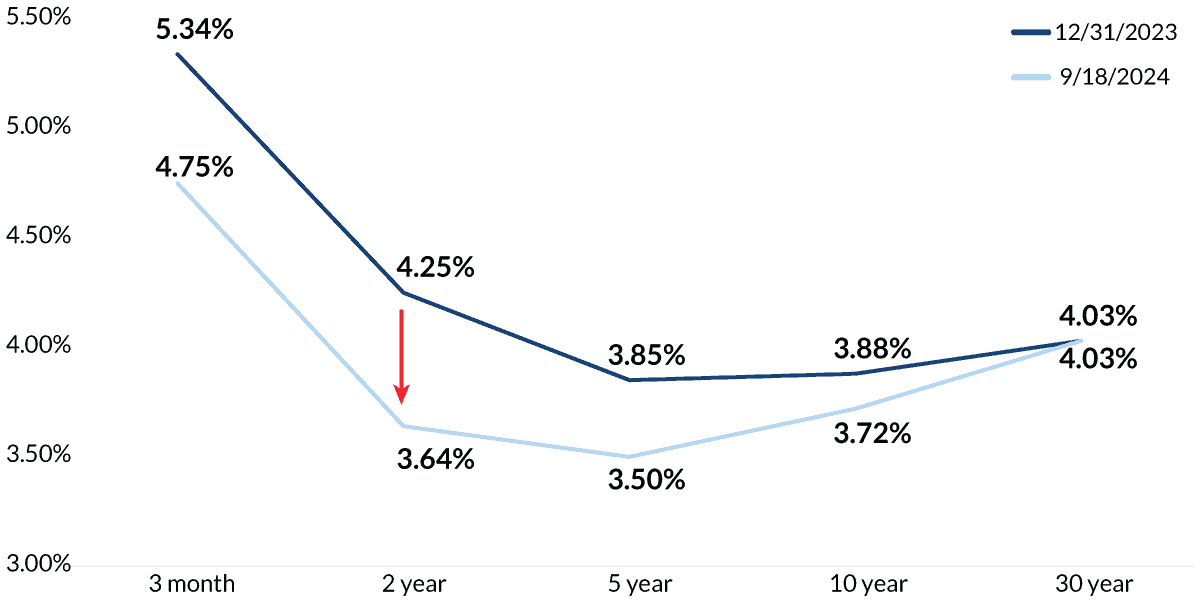

U.S. Treasury Yield Curve Changes YTD

Source: Bloomberg U.S. Treasury Index as of September 18, 2024.

Information is subject to change and is not a guarantee of future results

Chart 2, 1:58– In the weeks leading up to this change in Fed policy, yields across the Treasury curve had declined. As of this filming, 3-month and 2-year yields are lower by 60 basis points, while the 10-year is down a modest 16 basis points. Longer term yields remain unchanged.

Importantly, the slope between 2-year and 10-year yields has turned positive once again after inverting in 2022. We anticipate the curve to steepen further as treasuries with maturities within one year continue to fall with subsequent rate cuts, while sustained economic growth and supply pressures keep longer-term yields range bound.

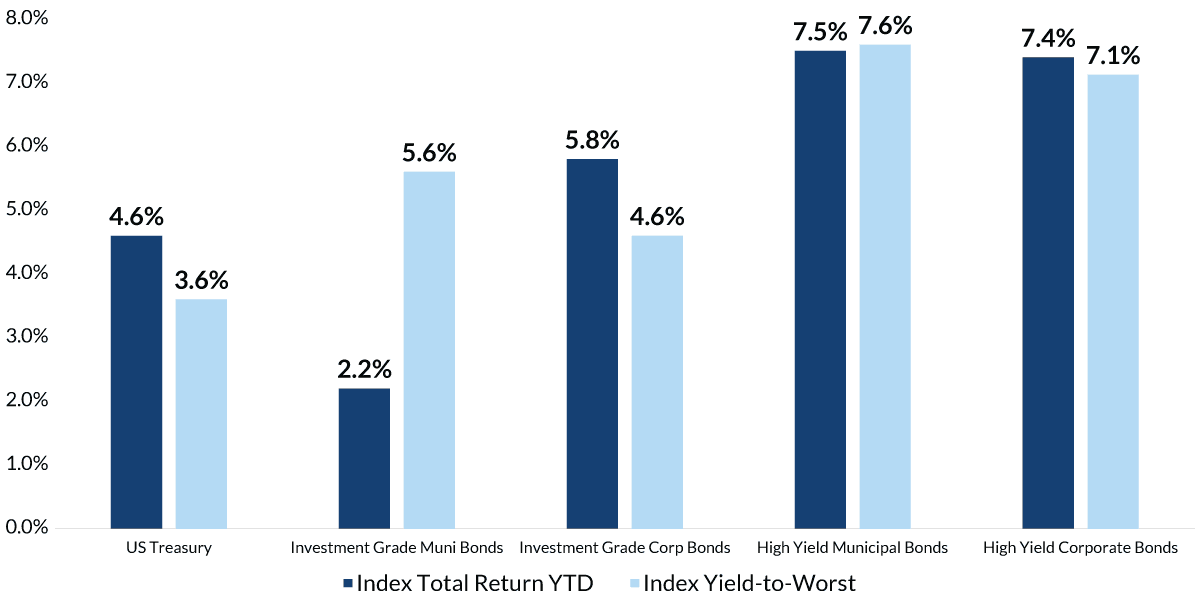

Fixed Income Asset Class Performance and Yields

Source: Bloomberg U.S. Treasury Index, Bloomberg Municipal Bond Index, Bloomberg Corporate Investment Grade Index, Bloomberg Municipal High Yield Index and the Bloomberg US Corporate High Yield Index ; investment grade and high yield municipal bond yield-to-worst is adjusted for 37% Federal tax rate + 3.8% Medicare Surcharge. All data as of September 18, 2024. Information is subject to change and is not a guarantee of future results.

Chart 3, 2:37– For fixed income investors, this has resulted in positive returns year-to-date, with investment grade sectors returning between 2% and 6% and high yield sectors 7.5%.

Both investment grade and high yield market sectors continue to look resilient with quality spreads near their recent lows, while record bond supply is being easily absorbed by investors who started to look further out on the curve to lock in attractive yields across the fixed income markets.

Important Information

The views expressed represent the opinions of City National Rochdale, LLC (CNR) which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While CNR believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Actual results, performance or events may differ materially from those expressed or implied in such statements. All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

City National Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise.

Fixed Income investing strategies & products. There are inherent risks with fixed income investing. These risks include, but are not limited to, interest rate, call, credit, market, inflation, government policy, liquidity or junk bond risks. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed income securities and during periods when prevailing interest rates are low or negative.

Index Definitions:

Bloomberg U.S. Treasury Index: includes all publicly issued, U.S. Treasury securities that are rated investment grade, and have $250 million or more of outstanding face value.

The Bloomberg US Municipal Bond Index measures the performance of investment grade, US dollar-denominated, long-term tax-exempt bonds.

The Bloomberg US Investment Grade Corporate Bond Index measures the performance of investment grade, corporate, fixed-rate bonds with maturities of one year or more.

The Bloomberg Municipal High Yield Bond Index measures the performance of non-investment grade, US dollar-denominated, and non-rated, tax-exempt bonds.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody's, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Bloomberg EM country definition, are excluded.

© 2024 City National Rochdale, LLC. All rights reserved.